Investment Thesis

Charlie Munger's original thesis remains relevant for the case of BYD Company Limited today. In 2008, Berkshire Hathaway purchased a 9.9% stake in BYD for roughly USD 232 million. Munger viewed the investment in BYD as an investment in the founder Wang Chuanfu's engineering culture when BYD was a pioneering battery company. Their long-term engineering focus in battery chemistry and sophisticated manufacturing processes is the foundation of their dominant position. In 2009, Charlie Munger noted:

"This guy (Wang Chuanfu) is a combination of Thomas Edison and Jack Welch — something like Edison in inventing new technologies and something like Welch in getting things done."

Their title as a vertically integrated company is often misunderstood. A significant amount of analysis has been done on BYD as an EV manufacturer, yet this does not capture the depth of their competency. BYD controls the critical 'midstream' steps — this covers lithium refining, LFP precursor preparation, cathode production, and cell manufacturing. This is a technical and political barrier for non-Chinese Auto OEMs (original equipment manufacturers). This moat has taken BYD over a decade to develop, allowing it to withstand competitive pressures from new entrants.

However, BYD's valuation has become disconnected from these strengths. When looking at a multiple valuation, BYD is trading at a discount to pure battery technology companies, at a premium when compared to pure Auto OEMs, and at a large discount to omni-channel technology Auto OEMs. In this consolidation period, we expect to see cash flow constraints. However, we determined BYD is better positioned to absorb such pressures than foreign/domestic competitors.

Business Overview

Minerals: The Real Value Is Conversion, Not Ore

The bottleneck in the global LFP (lithium ferrous phosphate) supply chain is not in mining but in conversion: lithium refining, precursor synthesis, cathode production, and cell manufacturing. These are the midstream conversion steps.

Lithium mining is geographically located across Australia, South America and Africa, yet the value created in the midstream conversion steps.. China accounts for 65-70% of global lithium capacity, 80-90% of active cathode production and 94% of the global LFP cathode supply. This is a core supply chain risk for non-Chinese Auto producers, and remains under-analyzed. The concentration has created a cost advantage that non-Chinese OEMs cannot access. Hunan Yuneng New Energy Battery Material Co., Ltd. and Hubei Wanrun New Energy Technology Co., Ltd. are leading Chinese producers of phosphate-based cathode materials (materials required in the preproduction phase of LFP batteries used in EVs). Their advantage is based on established factories that dominate the midstream segment. In 2025, China's industrial policy has further tightened export controls, reducing any meaningful chance of technology dispersion abroad.

Among China's battery dominant manufacturers, we identified BYD as being positioned uniquely to benefit from this political tailwind. While CATL (Contemporary Amperex Technology Co., Limited, a Chinese company specializing in lithium-ion batteries) and BYD operate in the midstream segment, only BYD processes their own LFP cathode material through their subsidiary FinDreams. CATL is subject to supply chain shocks through their purchase through third parties.

This level of integration at the granular level gives BYD a moat, aligns with China's industrial policy and strong supply chain resilience against foreign and domestic competitors.

Brownfield LFP Capacity: The Source of BYD's Cost Advantage

BYD's cost and utility advantage lies in its fully amortized midstream manufacturing base — its LFP factories and supply lines have already passed the heavy capital-intensive phase as they were built in 2018. BYD and CATL continue to expand this advantage through increased production and efficiency. CATL and BYD installed 151 GWh and 134 GWh of LFP capacity, respectively, in 2024. This reinforces their entrenched cost effective position.

Global Lithium supply continues to grow despite a 50% increase in demand in 2024. In 2022 amid a supply shortage, unstable lithium prices peaked above $80,000 and fell to just $9,000-12,000 per tonne by late 2025. This deflationary environment directly benefits vertically integrated companies like BYD, whose input costs fall immediately with falling input prices.

This volatility explains the divergence of strategy between competitors CATL and BYD. CATL is pursuing global expansion, shown by their $5.9 billion factory in Indonesia announced in 2025, to support a third-party model. BYD, by contrast, has terminated the proposed LFP cathode factory in northern Chile in 2025, signaling offshore lithium prices are increasingly uneconomic.

In short, the falling lithium prices, fully depreciated assets and wholly owned domestic supply chain subsidiaries leave BYD structurally positioned to maintain cost leadership in the near-term.

Cell-Level Advantage: Cost of Energy

BYD and other Chinese LFP producers have a widening cell-level cost advantage driven by structural and energy policies. In 2025, cell-level LFP cost was below $60 per kWh, while BYD achieved a further ~25% reduction through integrated cathode-to-cell production. In contrast, US LFP cells averaged over $94 kWh, while European production came in 30-50% higher. This gap reflects that the input components of foreign producers are at a structural disadvantage.

A key driver is energy policy. The cathode and anode synthesis stage in battery production is energy-intensive. European industrial electricity costs remain 40% higher than in China, eroding European manufacturing competitiveness.

Taken together, lower cost of energy and a fully integrated production base created a durable pricing floor for BYD, one unlikely to be matched by competitors. BYD's cost position and the country's energy policies create a defensible moat that should continue to strengthen.

The Cost of Safety: Why BYD's Battery Architecture Matters

Safety has become a competitive factor in China's EV market. BYD's Gen 2 Blade battery, an upgraded version of the company's long-cell LFP chemistry battery introduced in 2020, delivers a structural edge. Following a dramatic fire in Shanghai in October, Li Auto is recalling 11,411 of its flagship Mega MPV, half of their total sales. China records over 3,000 EV related fires each year, recent incidences of high-profile vehicles have brought safety and regulatory scrutiny in a highly competitive domestic market where many brands push rapid software-drive updates.

The Blade battery design addresses these risks. The long structure of the "blade" cells dissipates heat more efficiently, preventing the buildup of thermal spots within the pack structure. The cell-to-pack structure additionally is capable of stopping damage from spreading between cells. A safety test demonstration involving nail penetration, short circuiting and crushing of the battery pack while retaining core functionality.

As further battery-related accidents arise, manufacturers with proven safety records will be advantaged. BYD's measured pace is an advantage for China's intensifying regulatory policies. This reflects a focus on system-level thinking, engineering over marketing. The shift in stricter safety standards will be a tailwind and reinforces BYD's position as a market leader in hardware and safety.

Financial Analysis

China's EV market has entered into a consolidation phase similar to the solar panel industry in 2015. During the 2015 solar-module shakeout, aggressive pricing forced hundreds of firms out of the market consolidating the industry to three dominant firms. A similar pattern is emerging today. China had more than 500 EV brands in China in 2019, only 80 remain in 2025. This number is expected to further reduce to seven by 2030. A stricter regulatory environment will lead to the shakeout of weaker firms.

In Q3 2025, revenue reached RMB ¥566.3 billion for the first three quarters (+12.8% YoY), while net profit declined to RMB ¥23.3 billion (-7.6% YoY) and operating cash flow fell to RMB ¥40.8 billion (−27.4% YoY). Q3's net profit was RMB ¥7.82 billion. The decline in profitability is driven by higher R&D investments (+31% YoY) and slower domestic sales in product specific lines. BYD's balance sheet remains robust, shareholders equity rising to RMB ¥245.5 billion (+32.5% YoY) and monetary funds (cash and equivalents) of RMB ¥119 billion as of Q3 2025. Representing liquidity to sustain the consolidation cycle.

Despite soft headline deliveries, underlying indicators remain robust. Battery installations, which are a leading indicator of underlying global market share, increased from 16.2% to ~18% in 2025. This divergence suggest a mix-shift rather than market share erosion. Higher margin international sales begin to provide a meaningful offset. In the first 10 months of 2025, BYD registered 39,103 vehicles in the UK (+547.4% YoY, supported by expanded dealer coverage.)

Weakness in the Dynasty series (mainstream, mid tier) is consistent in the overcrowded mid-priced sedan category. The Ocean series (younger, value tier) and the FangCengBao Sub-Brand (off-road, premium tier) continue to scale, partially offsetting unit softness. This aligns with our assertion that BYD's structural competency is portfolio driven, rather than relying depending on a single category.

Beijing is prioritizing "high-quality" productivity which to lead to increasing margins in the long term for dominant players like BYD. BYD has positioned itself to benefit from this market bifurcation through established practices and structural investments. Since 2023, BYD has accelerated its model-development cycle to ~18 months from ~36 months, increasing car refresh rates and competitive price-performance offerings. Optimizing its dealer networks both domestically and abroad, reducing inventory drags by 20-25%. Expanded megawatt charging infrastructure (heavy duty fast charging network) to more than 4,000 units in 2025. We expect these investments to result in rising operating margins as BYD project 1.6-1.8 million vehicles in international sales.

As China's EV sector consolidates, BYD's scale, accelerated model development cycle and car dealership network will place it amongst the top brands that will strengthen rather than lose ground.

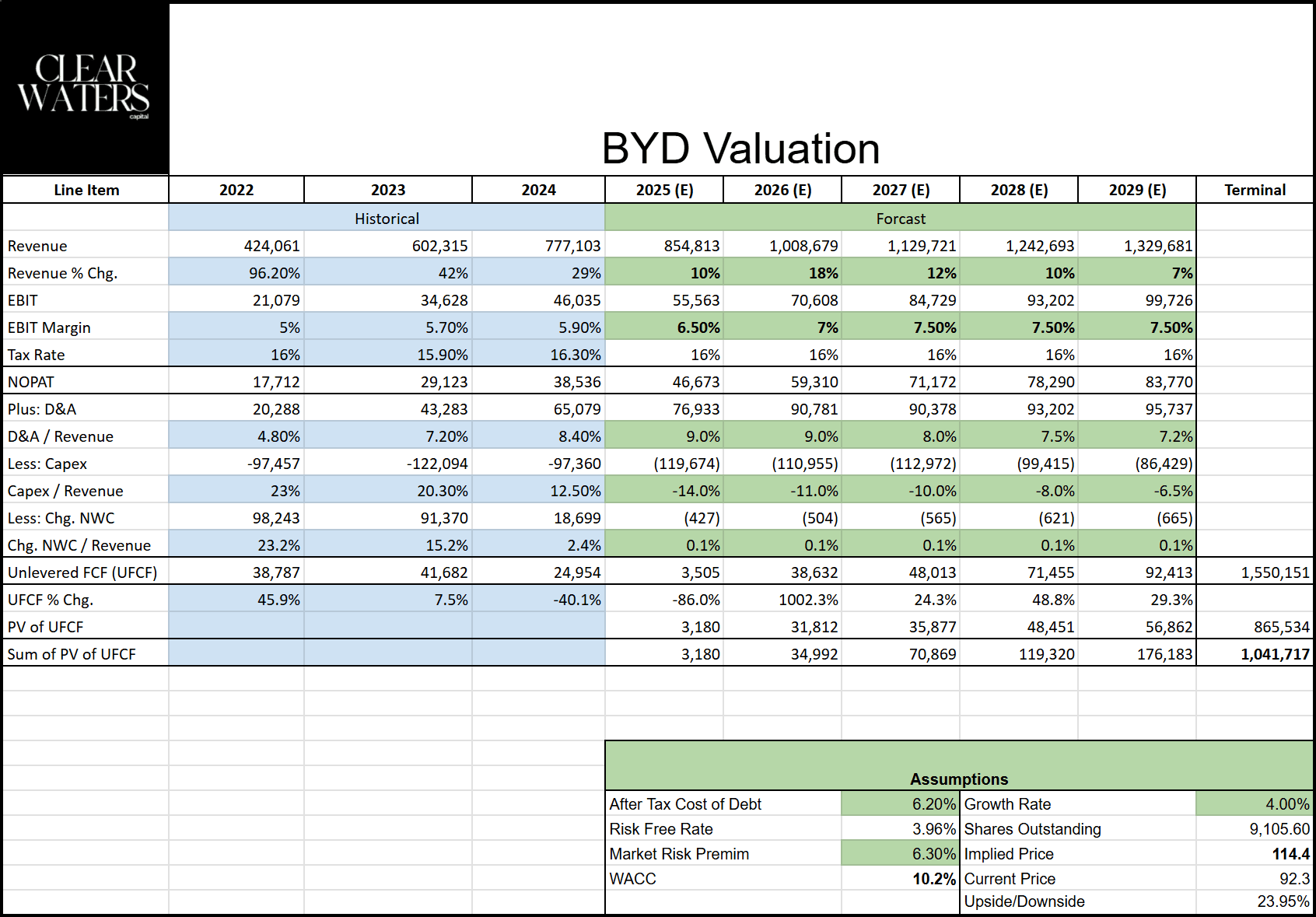

Valuation

BYD's current valuation does not accurately reflect the composition of its earnings. Despite its higher-margin vertical production mode, battery technology, and semiconductor business, the market maintains BYD as a misunderstood opportunity. The forward P/E of 17.3×, which is broadly in line with global auto OEMs, and the P/S of 1.03× indicate that the company is perceived as mature and do not reflect the true advantages of its vertically integrated production model.

Peer comparisons reveal a mismatch against companies with narrower production scopes. CATL trades at ~28.7× forward earnings and Xiaomi Corporation (XIACF) at ~18.4×. While Tesla, Inc.'s (TSLA) 181× multiple is not a useful benchmark due to several differences, including its perception as a fast-growing tech company and its margins in the mid 20's, among others. BYD's breadth across all segments of the supply chain is the result of deep investments in core competencies and self-reliance. There exists no single peer competitor that adequately reflects this combination of manufacturing segments. This mismatch contributes to the difficulty of valuation.

On a multiple valuation, we expect a re-rating to 20x forward P/E is conservative compared to the valuation of pure battery companies. This implies a ~18% upside from current levels.

Revenue growth has slowed from 42% in 2023 to ~9% in 2025, consistent with our description of the current domestic landscape. We assume a reacceleration towards mid-teens level growth as exports lift revenues from RMB ~¥847 billion in 2025 to ~RMB ¥1.2 trillion by 2029. A deliberately conservative trajectory below street expectations.

We expect EBIT margins to improve to 7.5% by 2029 driven by higher ASPs and contribution margins in international markets, easing domestic pressures and overall industry consolidation. Supported by overseas plants completing ramp-up. Under cautious DCF assumptions, applying a WACC of 10.2%, our valuation implies a meaningful ~20% upside with a price target of HK$114.4.

While we remain cautious about relying heavily on a Discounted cashflow model given the systemic risks in the auto landscape. We believe the market has already priced in the near-term volatility and cash flow compression. This situation makes the long-term valuation asymmetry more apparent.

Risks

Regulatory and Export Control Risk

As China tightens controls over certain advanced manufacturing processes, specifically cathode material and semiconductor manufacturing. BYD's position to capitalize on overseas factories could experience particular technology transfer limitations. This could raise the cost of engineering talent and diminish their cost advantage.

Battery Technology Risk

While BYD maintains its advantage with the Blade Battery Gen2 architecture, advances in solid-state and near-solid state batteries could reshape the technological landscape. This could put pressure on BYD's current hardware stack if these solutions achieve commercial scale.

Geopolitical and Trade-Policy Risk

Despite the overseas manufacturing lead that BYD commands over their Chinese counterparts in Thailand, Brazil and Hungry, increase uncertainty for China-EU relations could compress BYD's international margins.

Conclusion

The investment case for BYD returns to Munger's original insight: the company's edge is its engineering-first culture. BYD's vertical integration across mineral refining, precursor production, cell manufacturing creates a structural barrier non-Chinese OEMs cannot replicate. Competitors ultimately facing higher input costs, fragmented supply chains and are subject to stricter regulatory oversight in the transfer of technology.

These advantages are now structurally reinforced by China's industrial policy, self-reliance in high quality growth and regulatory tightening of safety standards. Combined together, these policies favor incumbents over unprofitable new entrants and foreign OEMs. BYD has long established themselves to benefit from strategic alignment with Beijing.

Taken together, the underlying fundamentals outlined above — regulatory tailwinds, midstream advantage, international sales, offers a strong directional clarity. Recent quarterly results show a temporary margin slowdown amid the heavy R&D investments in the international division, however, the structural advantage of BYD's business remain increasingly clear. For long term global investors, this creates a good opportunity to participate in a market leader in a global growing industry.

Key Catalysts

- International Sales Volume Ramp (2026): BYD expects 1.6-1.8 million international sales as production in foreign countries ramp-up. Overseas markets present a high ASP and healthier margins than the Chinese market.

- Midstream Efficiency Expands Cost Gap: As lithium prices remain deflationary, BYD's production along the midstream delivery improved margins while insulating them from possible supply shocks. Competitors relying on third-party producers such as CATL will experience a slow cost reduction.

- Regulatory Tailwinds on Technology and Safety: As Beijing finalize the 15th 5 year plan, which establishes the blueprint for self reliance and quality development. Increase scrutiny on rapid software innovation should reduce the competitive advantage of new entrants. More weight on stability and safety will allow BYD to defend their lead.