Investment Thesis

The bull case for BYD has not changed. The near-term picture has gotten harder, and that is the point.

BYD Company (1211.HK) enters 2026 under visible pressure: domestic market share fell from 25.4% in December to 15.8% in January, a price war with no defined end is eroding margins, and a government-mandated pledge to reduce supplier payment terms to 60 days carries an estimated USD 8–10 billion one-time cash flow hit. On reported earnings, the stock trades at roughly 11x a depressed earnings year. The thesis rests on what those reported earnings are hiding.

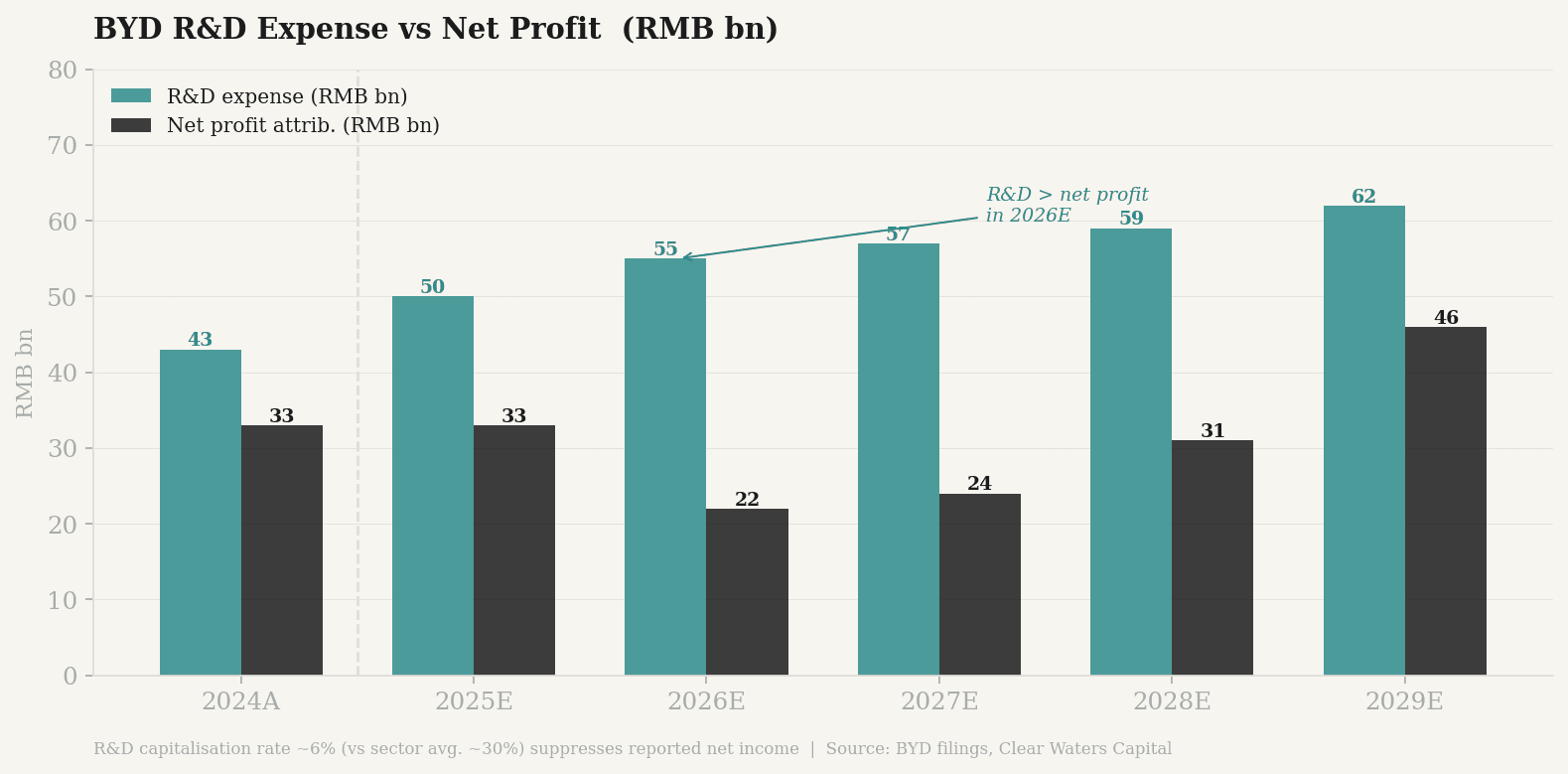

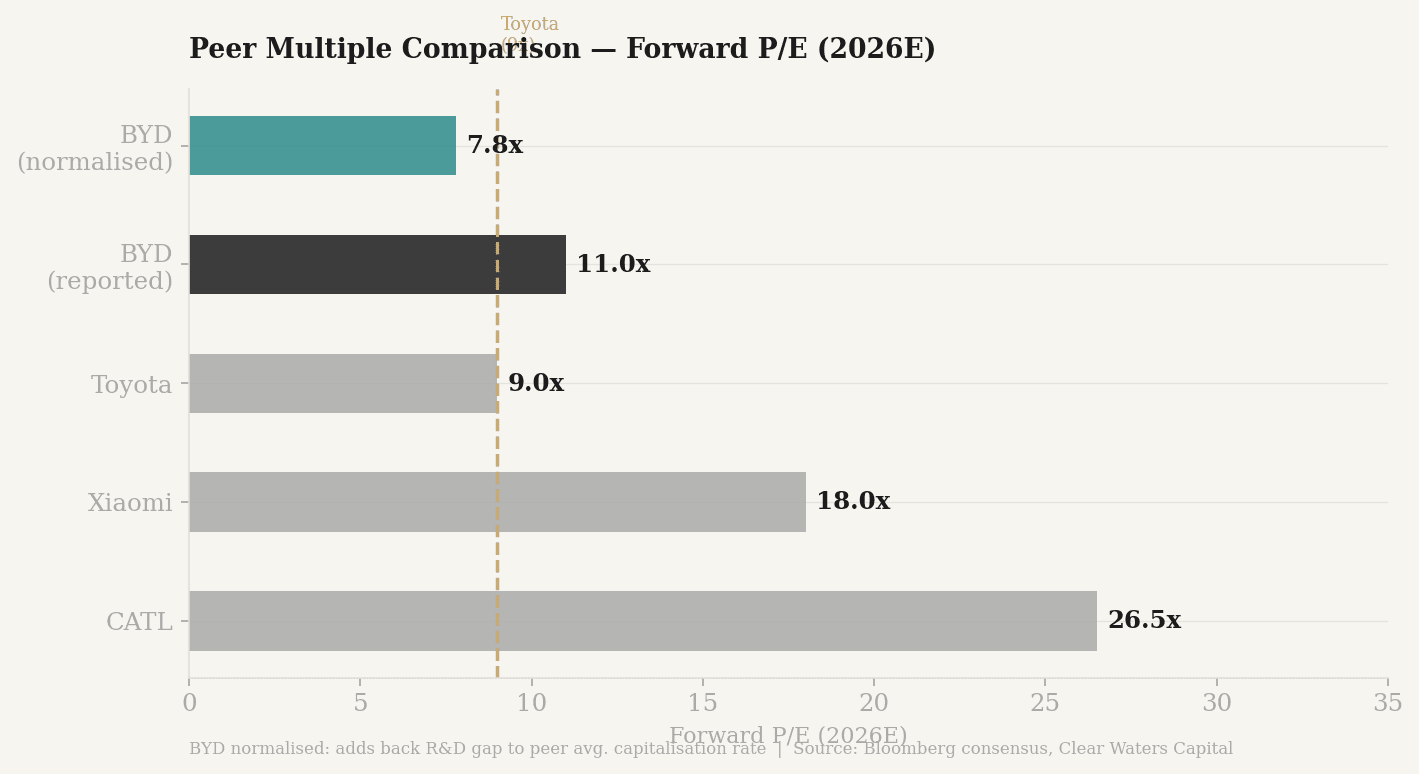

BYD capitalises only approximately 6% of its annual R&D spend. The sector average is 30%. The difference — roughly RMB 13 billion pre-tax in 2026 — flows directly into the expense line, suppressing reported net income by approximately RMB 10 billion after tax. Adjust for that accounting conservatism and the normalised multiple drops to approximately 7.8x: below Toyota, the world's most profitable automaker, which carries none of BYD's battery technology, energy storage business, or vertical supply chain integration.

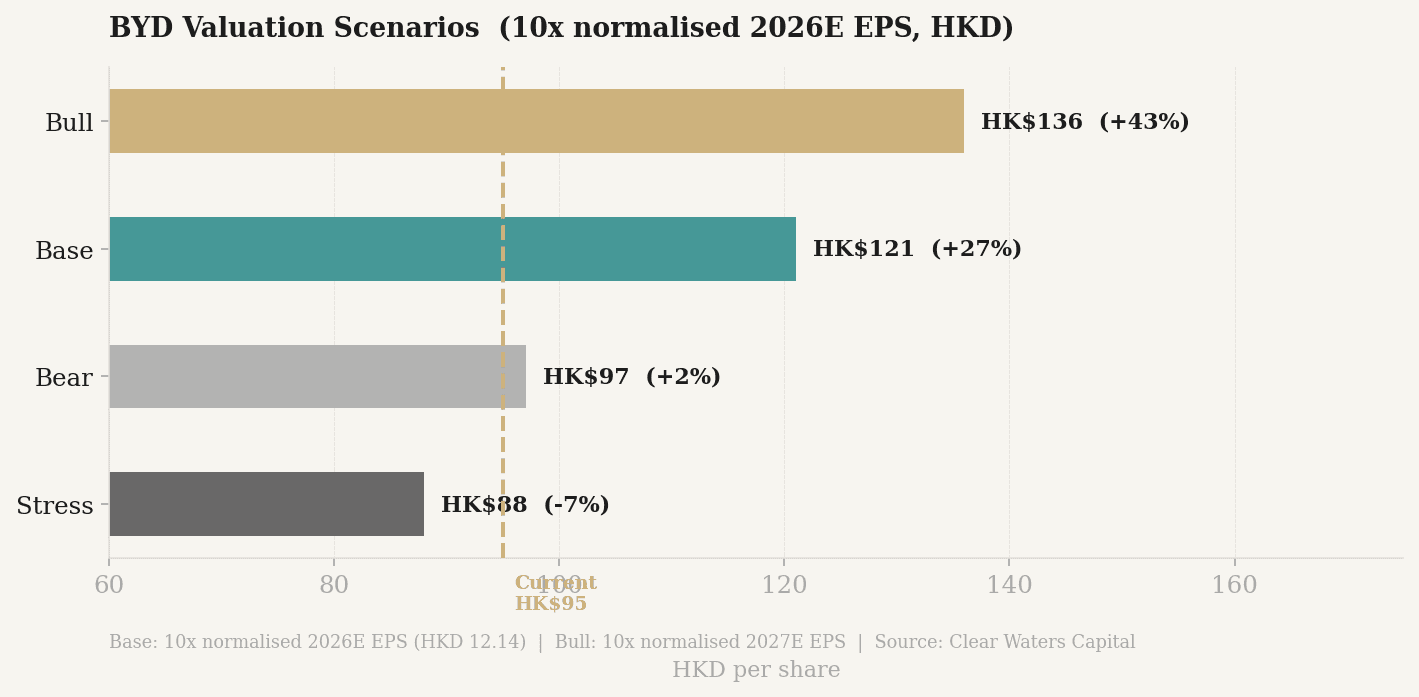

The asymmetry is straightforward. The bear case on our conservative model implies HK$97 — essentially the current price. The base case, at 10x normalised 2026 earnings, implies HK$121. The stress case, where margins stay compressed and revenue misses by 10%, implies HK$88, a 7% decline. Three of four scenarios are at or above current levels. The downside is narrow. The upside requires only that BYD survives a difficult two years with its balance sheet intact — which the RMB 57 billion cash position post-DPO compliance supports.

Price target: HK$121 (12-month base case). Rating: BUY.

Business Overview

Growth Driver 1 — The International Manufacturing Pivot

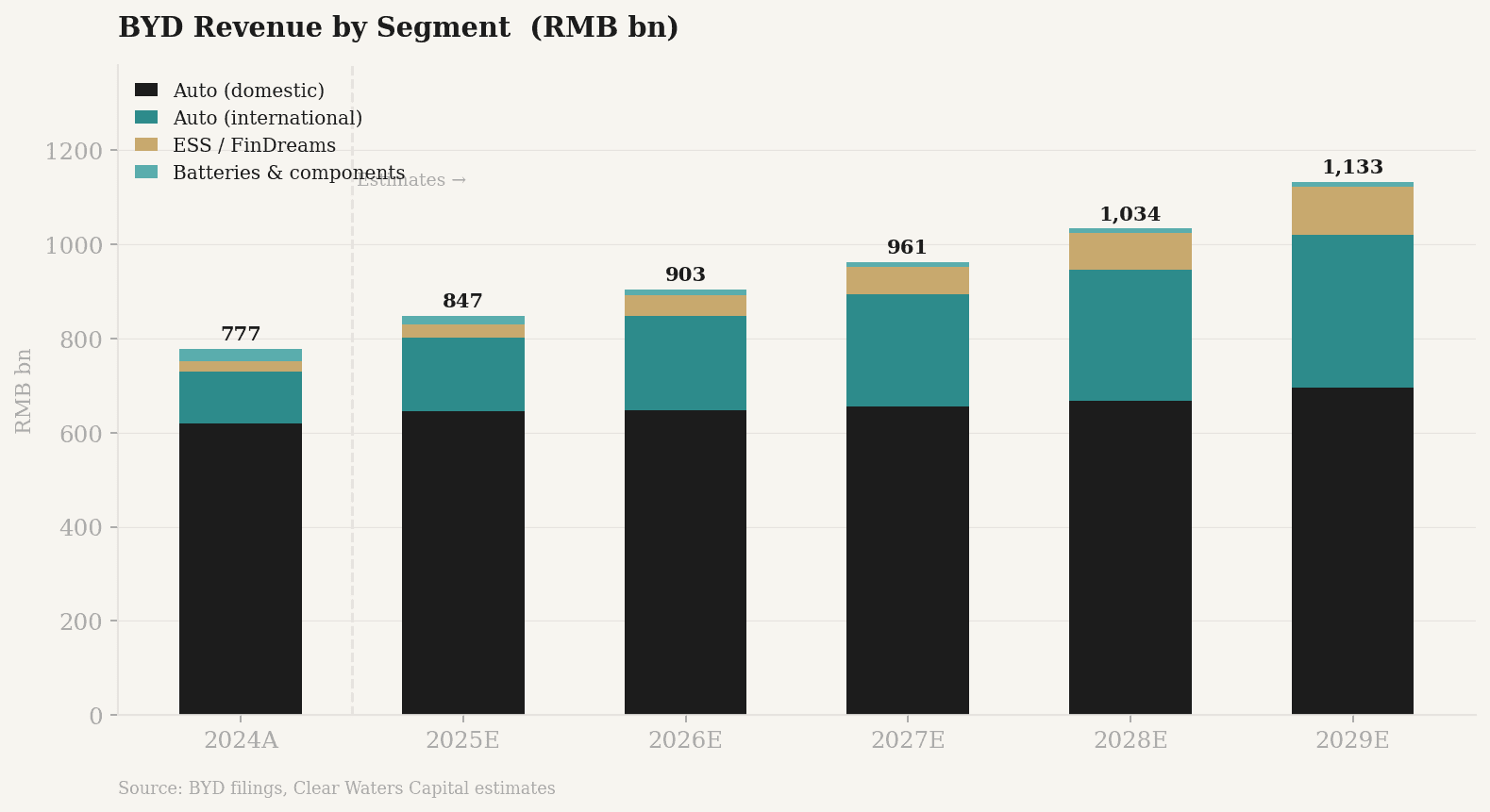

BYD exported 1.04 million vehicles in 2025, representing 29% of total group revenue at an average selling price approximately 40% above its China blended ASP. The international business is transitioning from an export model to a local manufacturing model — a structural shift that changes the margin profile of overseas sales once factories reach operating capacity.

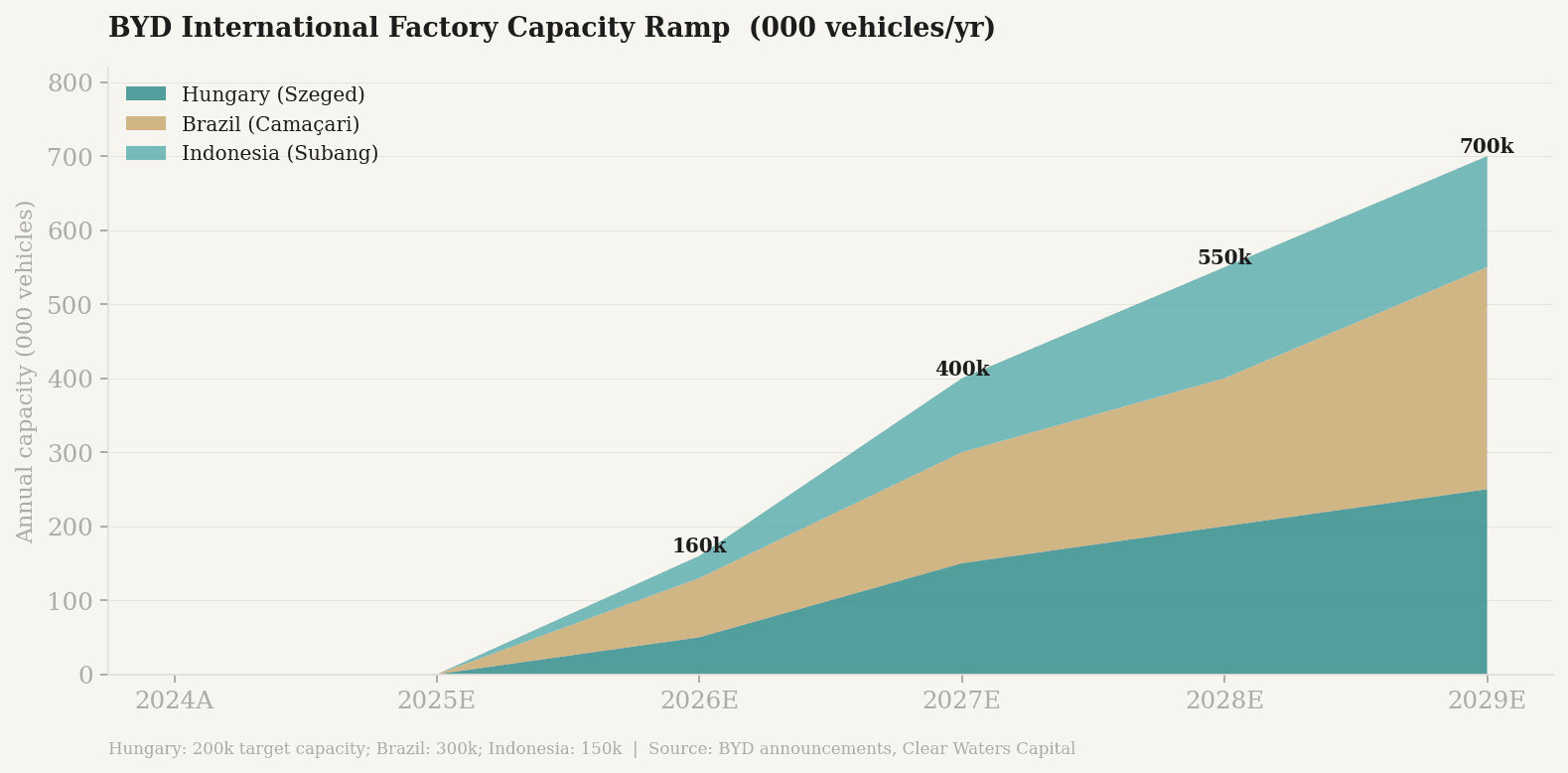

Hungary (Szeged): BYD's first European passenger car plant began trial production in January 2026, with mass production targeted for Q2. The facility is designed for 200,000 vehicles per year at full capacity, scaling toward 300,000 by 2030. Local production eliminates the European Commission's import tariff on Chinese EVs and positions BYD to meet the 70% local content threshold required for European state subsidy qualification — a threshold that competitors still exporting from China cannot meet. The strategic logic is not just cost; it is market access.

Brazil (Camaçari, Bahia): Built on a former Ford complex acquired at a fraction of greenfield cost, Brazil began assembling semi-knocked-down units in July 2025 while the stamping, welding, and painting facilities are completed. The SKD phase — importing pre-assembled kits and finishing locally — is a deliberate bridge strategy. It generates revenue immediately while local content builds toward the 50% threshold required by end-2026 to qualify for Brazilian import duty reductions. BYD is targeting 250,000 deliveries in Brazil in 2026, with capacity expanding to 300,000 annually to serve the broader Mercosur trade bloc. The plant carries execution risk: a USD 7.5 million labour settlement in late 2025 following an investigation into working conditions at the construction site was an unwelcome distraction, though it does not impair the long-term manufacturing case.

Indonesia (Subang, West Java): A USD 1 billion facility completing construction for a targeted 150,000-unit annual capacity. The Indonesian government granted BYD a temporary import duty exemption during the build phase — a recognition that local manufacturing creates domestic supply chain development — with the requirement that local content reaches 60% by 2026 to maintain the exemption. Indonesia is the entry point for BYD's Southeast Asian strategy, with longer-term export ambitions across the region.

The SKD model across all three markets reflects a consistent playbook: enter with volume immediately, build local supply chain relationships in parallel, and transition to fully local production as content thresholds are met. The margin uplift from local production — eliminating tariffs and reducing logistics costs — is a 2027–2028 event, not 2026. We model international auto revenue at RMB 200 billion in 2026 and RMB 238 billion in 2027, deliberately conservative against BYD's own 1.3 million unit guidance.

Growth Driver 2 — Energy Storage and Flash Charging

The energy storage business is the part of BYD that the headline P/E most completely ignores.

FinDreams and the ESS franchise: BYD's battery subsidiary FinDreams holds a 12% global share of energy storage cells, ranking second behind CATL, and a 32% share of the LFP energy storage market — the dominant chemistry for stationary storage — targeting 35% in 2026. The economics of ESS are structurally superior to automotive: longer contract durations, no dealer network, no warranty exposure comparable to vehicles, and cell-level cost advantages that non-integrated producers cannot replicate.

The FinDreams and Tesla relationship is the clearest evidence of this position. FinDreams supplies more than 20% of the cells for Tesla's Shanghai Megapack factory — approximately 8 GWh per year — generating an estimated CNY 3.5 billion in annual revenue. BYD won the contract by pricing near production cost, which a vertically integrated producer can sustain where third-party cell manufacturers cannot. The relationship is strategic as much as commercial: BYD supplies the cells that go into a competitor's energy storage product, sold globally, because BYD's cost floor is below the market clearing price.

We model ESS external revenue at RMB 43 billion in 2026, growing to RMB 103 billion by 2029. The growth rate — approximately 55% in 2026, moderating to 30% by 2029 — reflects both the FinDreams base and BYD's expanding utility and commercial storage contracts in Europe and Southeast Asia. ESS gross margins are estimated at 24% in 2026, expanding as the scale of fixed-cost cell production is spread across more contracts.

Flash Charging: In March 2026 BYD launched its Flash Charging network with 4,239 stations live at launch across China, targeting 20,000 by year-end — 18,000 urban co-location sites and 2,000 highway stations, with the first 1,000 highway locations opening before May 2026. At 1,500 kW peak output per gun, it is the most powerful mass-produced charging infrastructure deployed at scale.

The architectural innovation is not the charging speed — it is the integrated 200–300 kWh battery buffer built into each charging pile. The buffer draws slowly from the grid over hours and discharges at megawatt speed when a vehicle connects, bypassing the grid capacity upgrade that is the primary cost and timeline bottleneck for high-power charging infrastructure globally. The result is an installation cost approximately 60% below conventional megawatt charging approaches. BYD plans to extend Flash Charging internationally by end-2026, beginning in Hungary, Brazil, and Southeast Asia — markets where it already has manufacturing presence and fleet relationships.

The charging network is not modelled as a standalone revenue line at this stage. Its strategic value is in reducing the total cost of EV ownership for BYD vehicle buyers in BYD's key international markets, accelerating adoption ahead of the factory ramp.

Growth Driver 3 — Consolidation Survivor

China had more than 500 EV brands in 2019. Approximately 80 remain in 2025. The consensus projection is seven by 2030. The consolidation is not yet complete, and the ghost brands — loss-making but still producing, often supported by local governments seeking to protect employment — are keeping pricing pressure elevated across all volume segments. This is the primary near-term headwind.

It is also the medium-term tailwind. BYD entered 2026 with RMB 128 billion in cash and is one of the only major domestic EV producers running positive operating cash flow at current pricing. Its fully amortised midstream LFP manufacturing base — lithium refining, cathode production, and cell manufacturing built out since 2018 — means the cost floor is below where most competitors can profitably operate. When a competitor exits, the volume, dealer relationships, and fleet contracts flow toward the survivors. BYD is the most likely primary beneficiary of that consolidation in the volume and commercial segments, even as the premium segment remains contested.

Financial Analysis

The financial picture for 2026–2027 is intentionally conservative.

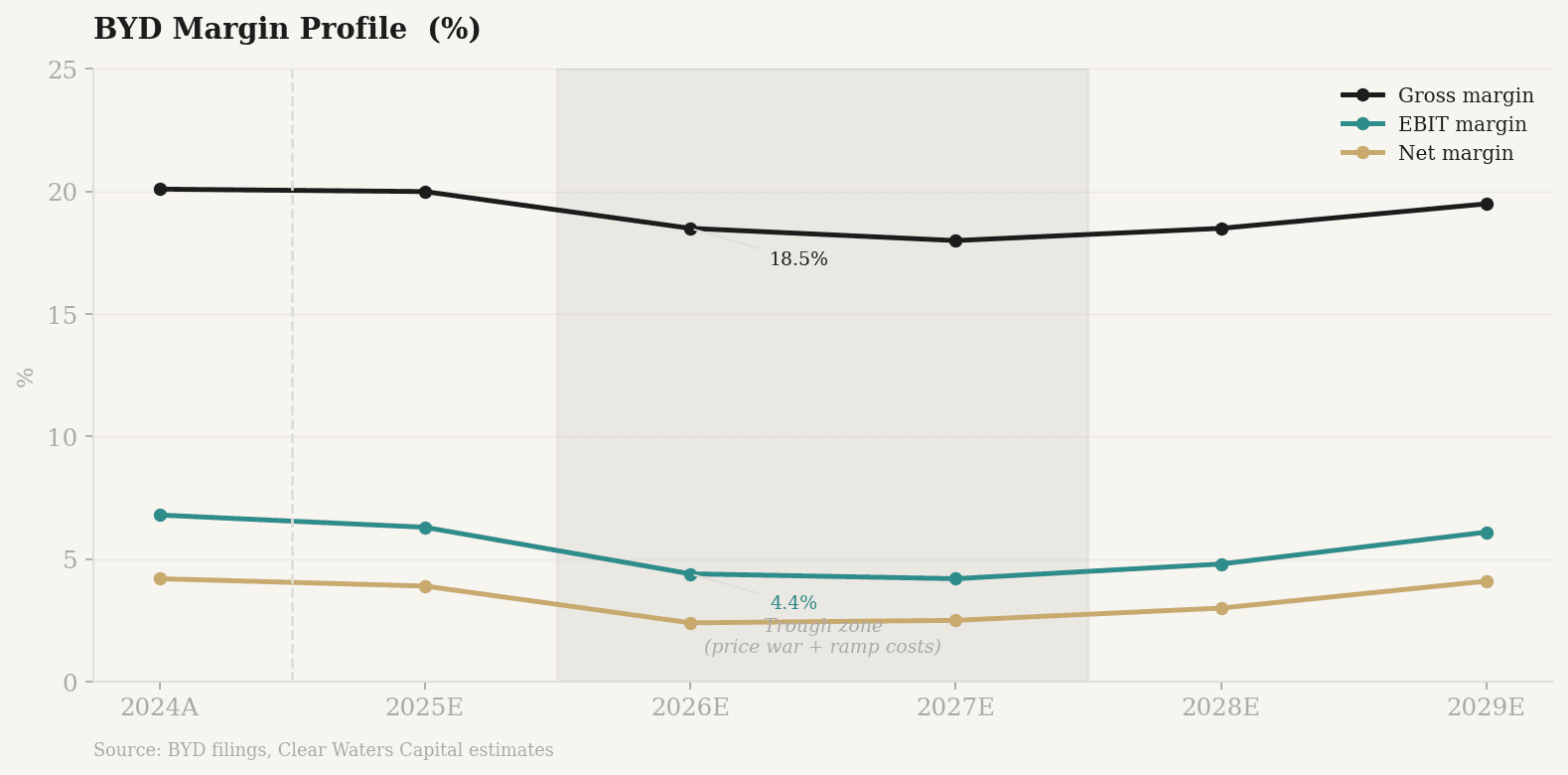

Revenue grows at 7% in 2026 and 6% in 2027 — a sharp deceleration from the 23% reported in 2024. Gross margin compresses to 18.5% in 2026 and 18.0% in 2027 as domestic price pressure and international factory ramp inefficiencies overlap. Net margin falls to 2.4% in 2026, recovering only modestly to 2.5% in 2027. R&D investment holds at approximately 6% of revenue, peaking at RMB 57 billion in absolute terms as BYD continues developing God's Eye ADAS, the DiPilot platform, and in-house chip design.

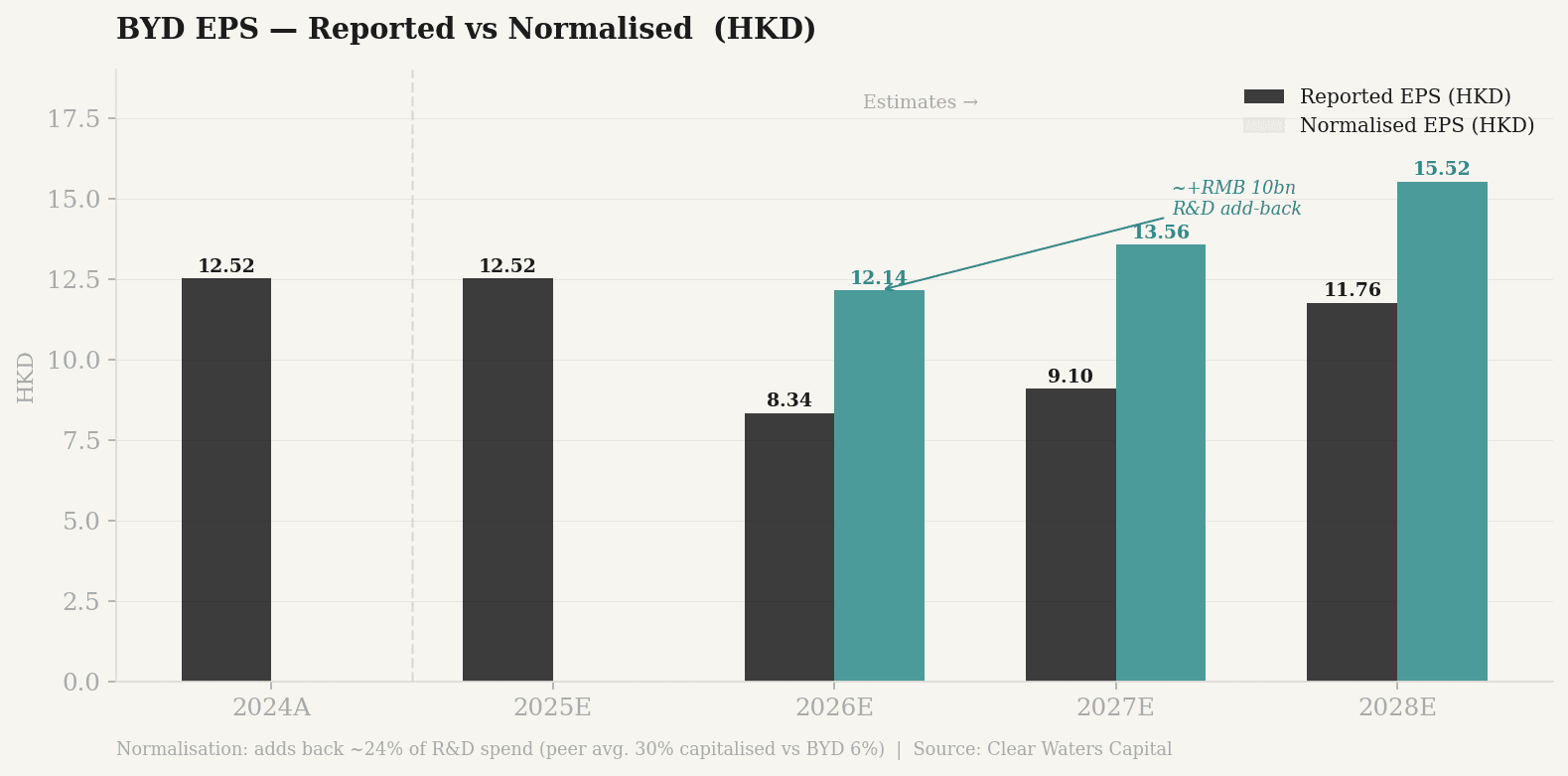

Reported EPS falls from HKD 12.52 in 2025 to HKD 8.34 in 2026 — a 33% decline driven by the convergence of DPO compliance, margin compression, and elevated capex. Recovery is gradual: HKD 9.10 in 2027, HKD 11.76 in 2028.

The normalised picture is more stable. BYD capitalises only approximately 6% of R&D against a sector average of 30%. Adding back the gap — roughly RMB 13 billion pre-tax, RMB 10 billion after tax — raises normalised net profit from RMB 22 billion to RMB 32 billion in 2026, and normalised EPS from HKD 8.34 to HKD 12.14. The reported earnings decline is substantially a function of conservative accounting applied to a high and growing R&D base, not underlying business deterioration.

Free cash flow turns negative in 2026 — approximately RMB 71 billion — driven by the DPO compliance one-off hitting operating cash flow. BYD enters 2026 with RMB 128 billion in cash. Post-compliance, the balance sheet holds approximately RMB 57 billion, sufficient to fund operations and the ongoing international factory build without distress.

Valuation

BYD on normalised 2026 earnings trades at approximately 7.8x — a discount to Toyota (9x reported), well below Xiaomi (18x), and a fraction of CATL (25–28x). No peer carries BYD's combination of vertical supply chain integration, energy storage market share, international manufacturing footprint, and growing charging infrastructure.

The base case applies 10x to normalised 2026 EPS of HKD 12.14, implying HK$121 — 27% above the current price. No recovery is assumed. No multiple expansion is assumed. The requirement is only that BYD navigates 2026 with its balance sheet intact.

The bull case — 10x normalised 2027 earnings of HKD 13.56 — implies HK$136, a 43% return requiring domestic stabilisation and Hungary contributing meaningfully to group revenue. The bear case at 8x normalised 2026 earnings implies HK$97. The stress case — margins compressed, revenue 10% below model — implies HK$88. Three of four scenarios are at or above the current price.

Position sizing: 4% of portfolio at current levels. Add to 6% at HK$80 with thesis intact. Full position at HK$75 — the Burry floor.

Risks

ADAS gap — the primary structural risk. BYD is categorised as a Tier 3 provider in city Navigate on Autopilot, behind Huawei (Tier 1), Xpeng (Tier 1), and Xiaomi (Tier 2). In the CNY 200,000–300,000 segment — the highest-margin category in the domestic market — BYD fell out of the top five brands in both 2024 and 2025. The Tang L and Han L, launched in April 2025 as BYD's premium ADAS flagships, were poorly received. Sales of the Tang fell 68.6% year-on-year by February 2026. The product refresh with new software architecture is delayed until late 2026. Until independent benchmarks confirm God's Eye DiPilot in Tier 2 or above, the premium domestic segment remains structurally impaired and the margin mix reflects it.

DPO compliance — a one-time but significant cash event. BYD's historical supplier payment terms averaged 155 days, extending in some cases to 275 days. The June 2025 industry pledge sets a 60-day maximum. BYD has publicly committed to compliance and management argues that 70% vertical integration neutralises the impact — BYD both pays and receives within the new framework. Analysts estimate the one-time cash outflow at USD 8–10 billion regardless. The FY2025 annual report, due April 2026, will provide the first quantified disclosure of compliance progress. If cash falls below RMB 80 billion and compliance has already begun, the thesis timeline extends materially.

International factory ramp slippage — an execution risk with a long tail. Turkey has already been cancelled. Hungary, Brazil, and Indonesia are all operating on aggressive timelines that carry real execution risk. Hungary's mass production date of Q2 2026 has not been confirmed at scale. Brazil's 250,000-unit 2026 delivery target is ambitious given that full local stamping and painting facilities are still being commissioned. Indonesia faces a rising local content threshold — 60% by 2026 — that requires rapid supplier development in a market with limited EV supply chain depth. If two of the three factories slip by 12 months or more, the international margin uplift that underpins the 2027–2028 recovery does not materialise on schedule and the bull case moves to 2029.

Conclusion

BYD in March 2026 is a harder story to tell than it was in November 2025. The domestic data is ugly. The margins are under pressure. The ADAS gap is confirmed and wider than hoped. The DPO cash hit is coming.

It is also, on the numbers, cheaper. Normalised earnings are closer to HKD 12 than the reported HKD 8. The balance sheet is intact. The international factories are live and building toward the tariff-free, locally-produced margin structure that makes the overseas thesis work. The ESS business is growing at 55% annually into a market where BYD's cell cost advantage cannot be replicated by non-integrated competitors within a five-year horizon. The consolidation cycle is running in BYD's favour across every segment except the premium domestic tier — and that is a product cycle problem with a known resolution date.

What to watch in the next 12 months:

FY2025 annual report (April 2026): The most important near-term data point. Watch the DPO line — specifically whether compliance has begun and what the cash position implies for the one-time hit. Watch overseas segment margins for the first time disclosed separately.

Domestic market share (March–May 2026): January and February were seasonally distorted. Market share needs to recover toward 20%+ by May to confirm that the domestic decline was seasonal rather than structural. If it does not, the ADAS risk moves from watch to exit consideration.

Hungary production ramp: Full production targeted Q2 2026. A delay beyond Q4 pushes the international margin story to 2028 and lengthens the investment timeline.

God's Eye ADAS benchmarks (H1 2026): If DiPilot 600 benchmarks place BYD in Tier 2 against Huawei and Xpeng by mid-year, the primary structural risk is closing. If it remains Tier 3, reduce the position on any rally above HK$110.

Munger's original insight was not about BYD the automaker. It was about Wang Chuanfu's engineering culture — the willingness to invest through difficult periods without cutting corners. That culture is visible in the R&D line, which has not been reduced despite earnings pressure. It is visible in the Flash Charging buffer architecture, which solves a grid capacity problem that competitors have been deferring. It is visible in the decision to build factories across three continents rather than export indefinitely.

The reported earnings are the floor. The normalised earnings are the thesis. The entry is now.