Investment Thesis

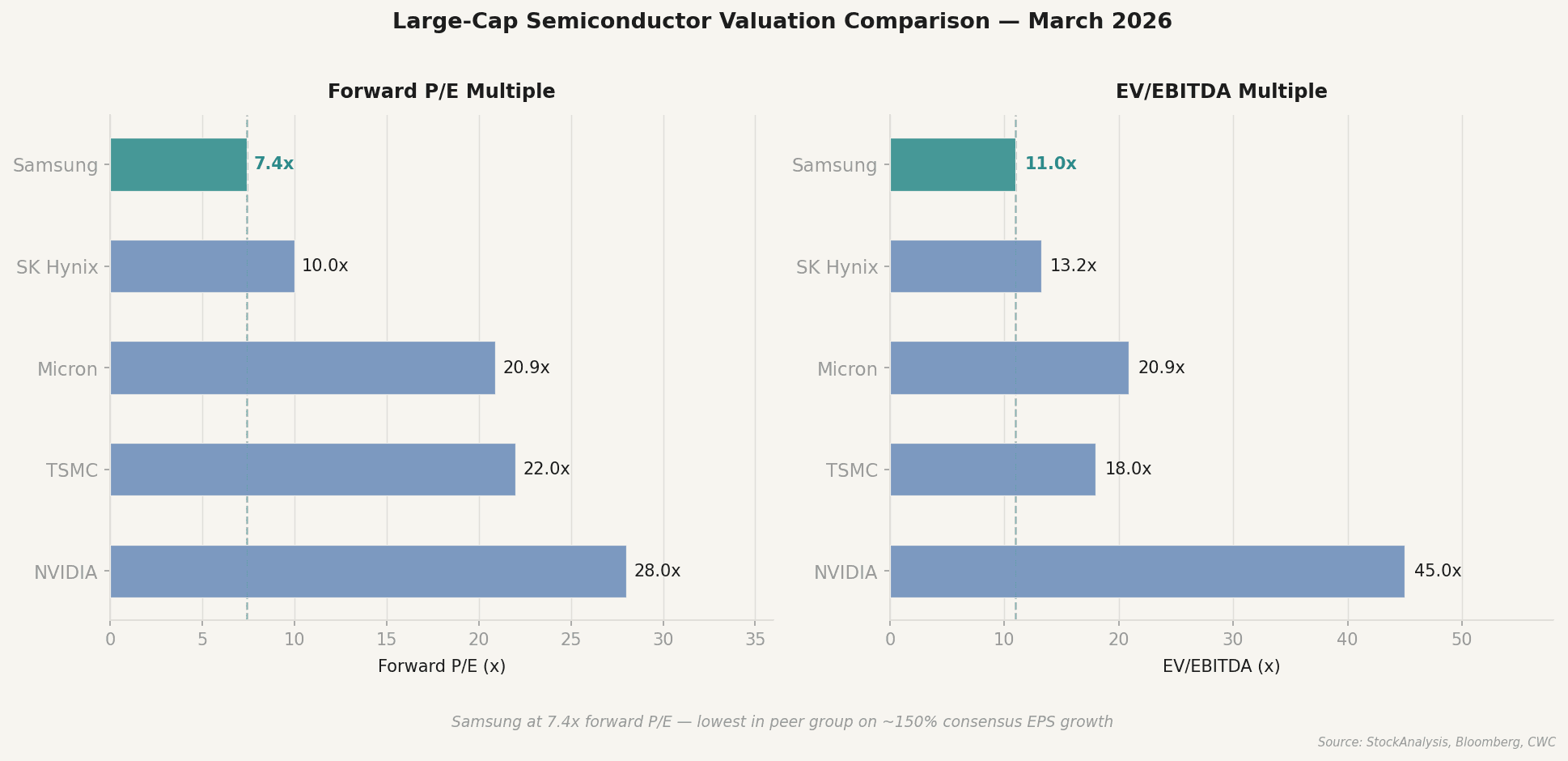

The prolonged US-Iran war triggered the worst two-day KOSPI selloff in history on March 3–4, with further selloffs continuing today, hitting every Korean blue chip indiscriminately. This created a significant price drop from the February 27 highs. The core investment case remains intact: Samsung Electronics (KRX:005930 / OTC:SSNLF) trades at approximately 7.4x forward P/E based on strong 2026 consensus earnings growth.

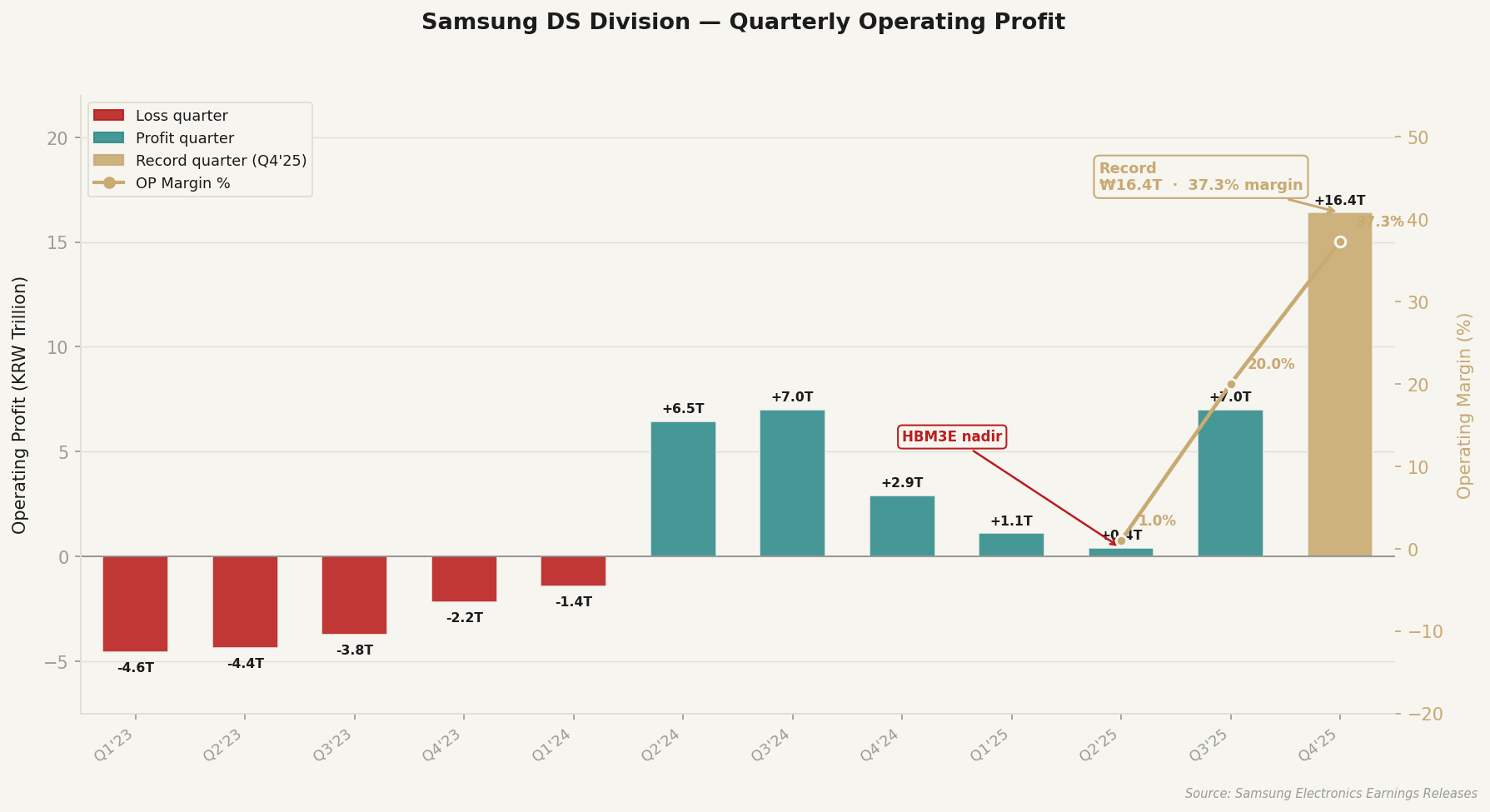

The market appropriately penalized Samsung for its struggle with HBM3E, during which SK Hynix overtook them in annual operating profit. Following that failure, commercial HBM4 shipments have now begun. Samsung's vertical integration provides a unique cost advantage, and its conventional DRAM business currently generates cash at highly elevated margins. We have a buy rating at KRW 240,000; we believe the risk profile is attractive, and the current geopolitical tensions will create a good entry point.

Why Now

The past 75 days have created a distinct entry window, driven by four key factors:

- Commercial HBM4: Samsung began paid commercial HBM4 shipments on February 12, 2026.

- Korea Discount Reforms: South Korea passed mandatory treasury share cancellation legislation on February 25, addressing long-standing valuation issues.

- Tax Exemptions: A domestic tax exemption program launched in December 2025 has driven sustained inflows from Korean retail investors, pushing prices up through February.

- Geopolitical Sell-Off: Recent US-Israeli strikes on Iran caused a historic KOSPI crash. Because Samsung's internal yields and long-term roadmaps were unaffected by the geopolitical shock, this created a compelling entry point at KRW 173,500.

Business Overview

Samsung's vertical integration provides a unique cost advantage across memory, foundry, consumer electronics, and displays. Unlike the fabless/foundry model dominant in logic chips, Samsung designs, manufactures, packages, and sells its own chips — the structural foundation that makes every thesis driver below possible.

Financial Analysis

Driver 1: HBM4 Recovery

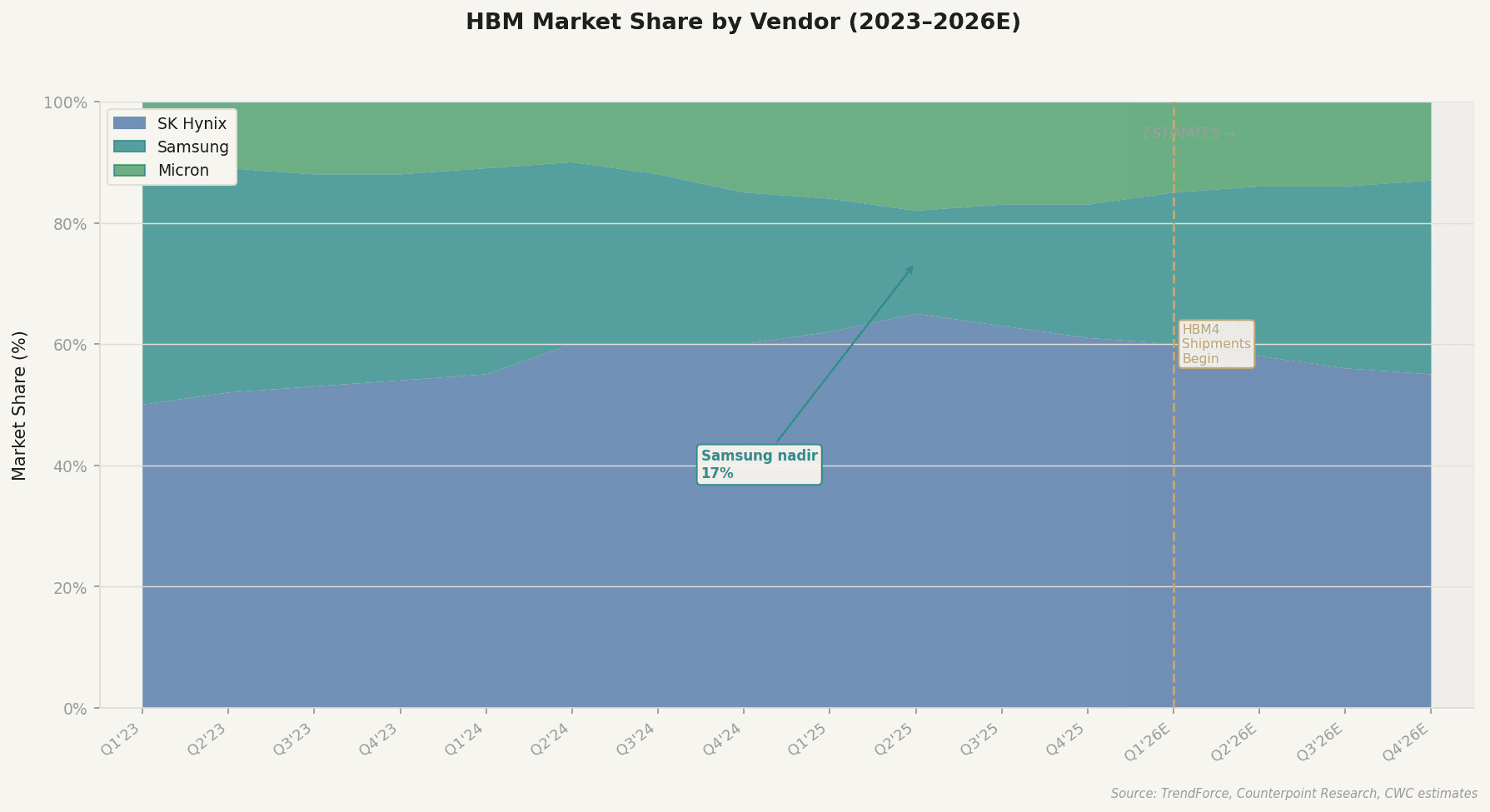

A failure in thermal design during the HBM3E generation led to extended NVIDIA qualification delays, collapsing Samsung's HBM market share to 17% by mid-2025.

Instead of dwelling on this, Samsung quickly pivoted to Google's TPU. While their HBM3E struggled with NVIDIA's brute-force environments, it operated reliably within Google's tightly controlled infrastructure. This pivot successfully secured over 50% of Broadcom's HBM supply for Google's Ironwood TPU.

Looking forward to NVIDIA's Vera Rubin platform (HBM4, H2 2026), Samsung is targeting a base-case 20% share of the allocation. With global HBM demand surging, Samsung's 2026 HBM supply is already fully committed.

Driver 2: Integrated Architecture — A Complex Cost Advantage

HBM4 requires the base die to migrate from conventional DRAM to an advanced logic node. Samsung is taking the ambitious route of fabricating all HBM4 layers (DRAM, logic base die, and advanced packaging) internally. Competitors like SK Hynix and Micron must outsource the base die to TSMC. Samsung's IDM approach allows them to capture the margin — estimated at ~30% — that competitors pay to TSMC.

This internal approach carries high technical risk. Micron attempted to design its own base die without TSMC, failed heat dissipation tests, and missed the 2026 Rubin qualification window, forcing them to partner with TSMC for future iterations. Samsung chose to go it alone to protect its margins, achieving an HBM4 stack running at 13 Gbps.

However, yielding these complex stacks at scale remains a hurdle. If internal yields fail, they deliver less supply, which simultaneously squeezes the market resulting in higher prices, while hampering Samsung's ability to fulfill commitments.

Driver 3: Conventional Memory Cash Engine

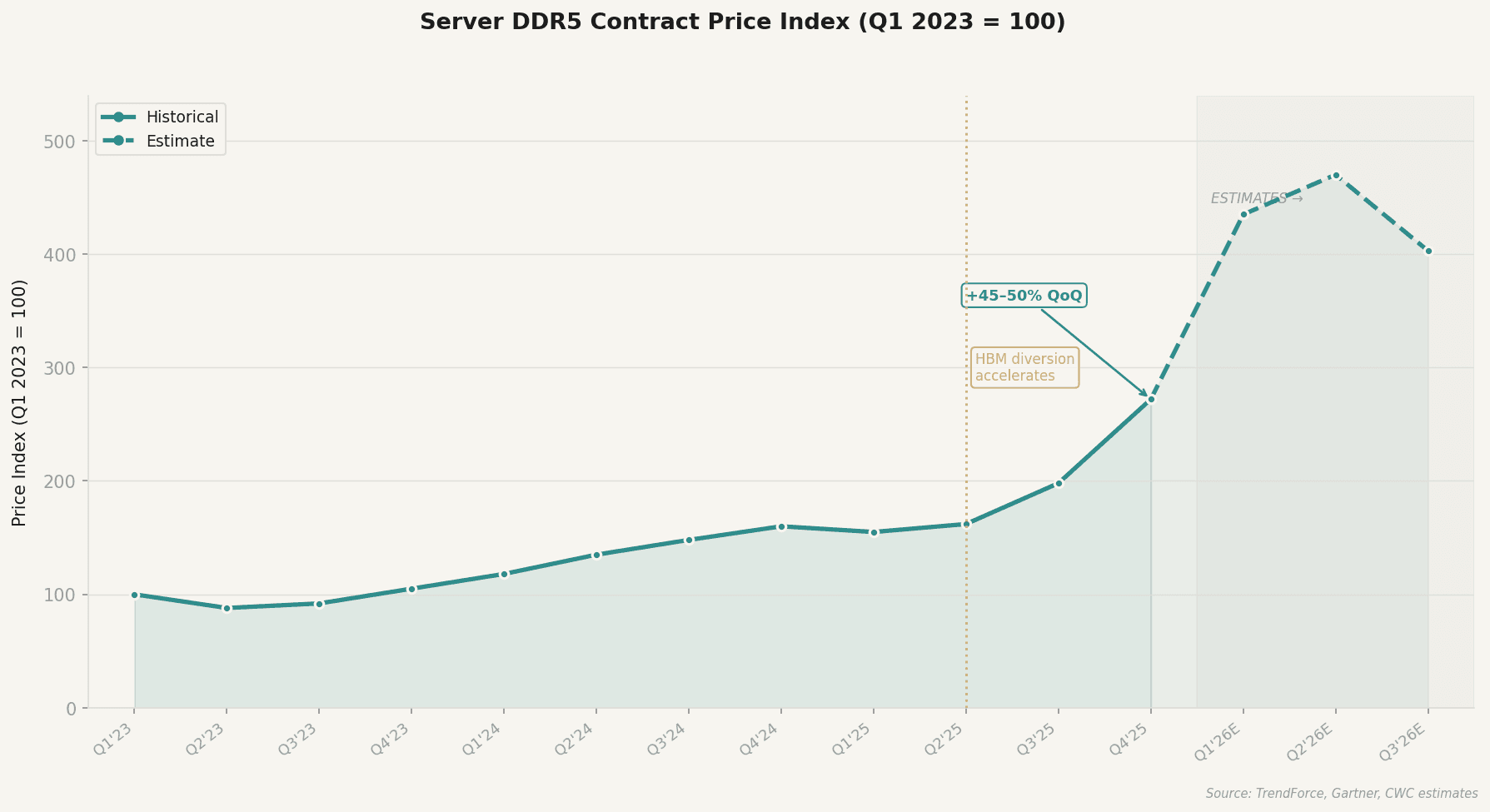

Conventional DRAM is funding this HBM transition. As competitors rushed to convert factory capacity to HBM, standard DDR5 supply tightened. Samsung intentionally maintained conventional capacity to exploit this squeeze.

Currently, a 64GB DDR5 server module commands roughly 70% gross margins. Since one HBM4 stack requires 3–4x more wafer space than DDR5, conventional DRAM remains highly profitable per wafer.

China's CXMT is aggressively targeting the legacy DRAM market, meaning Samsung's price advantage on standard DRAM might only last another year. However, Samsung has shielded itself in the short term by aggressively utilizing NCNR (non-cancellable, non-returnable) forward contracts, locking in high pricing for 2026.

What the Market Is Missing

Consensus hasn't fully appreciated Samsung's diversified revenue base. As custom ASIC chips like Google TPU capture more AI spend, Samsung's pivot to these customers provides a distinct advantage. Furthermore, the Korean repatriation tax program provides sustained domestic buying pressure. The recent geopolitical noise simply created a possible re-entry point for investors.

Valuation

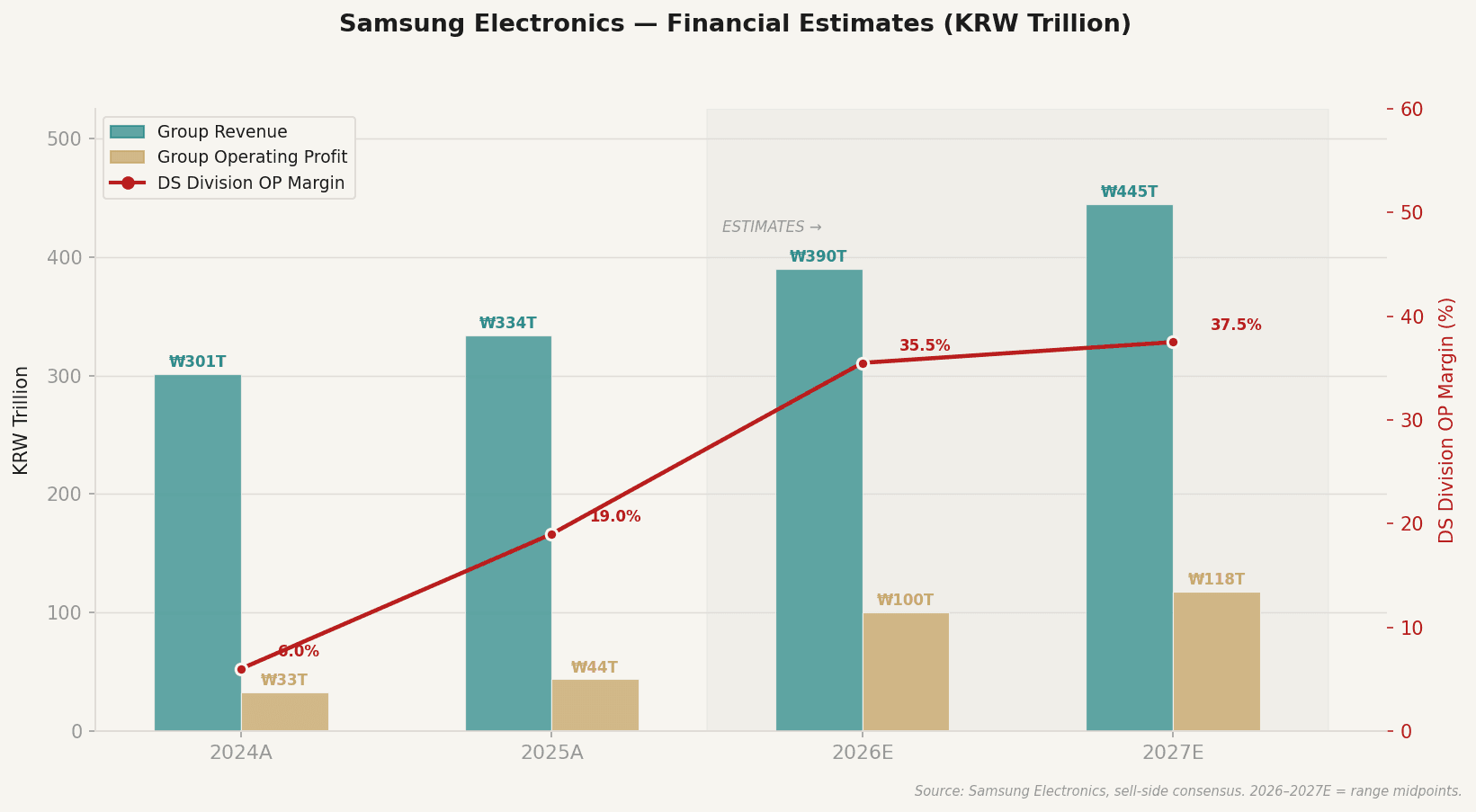

Samsung trades at an optically low forward P/E due to rapid, cyclical earnings growth this year. Memory revenues and margins will eventually moderate in the coming years. However, the core thesis is that AI demand has structurally shifted the cycle, establishing a durably higher earnings floor for Samsung during future market troughs.

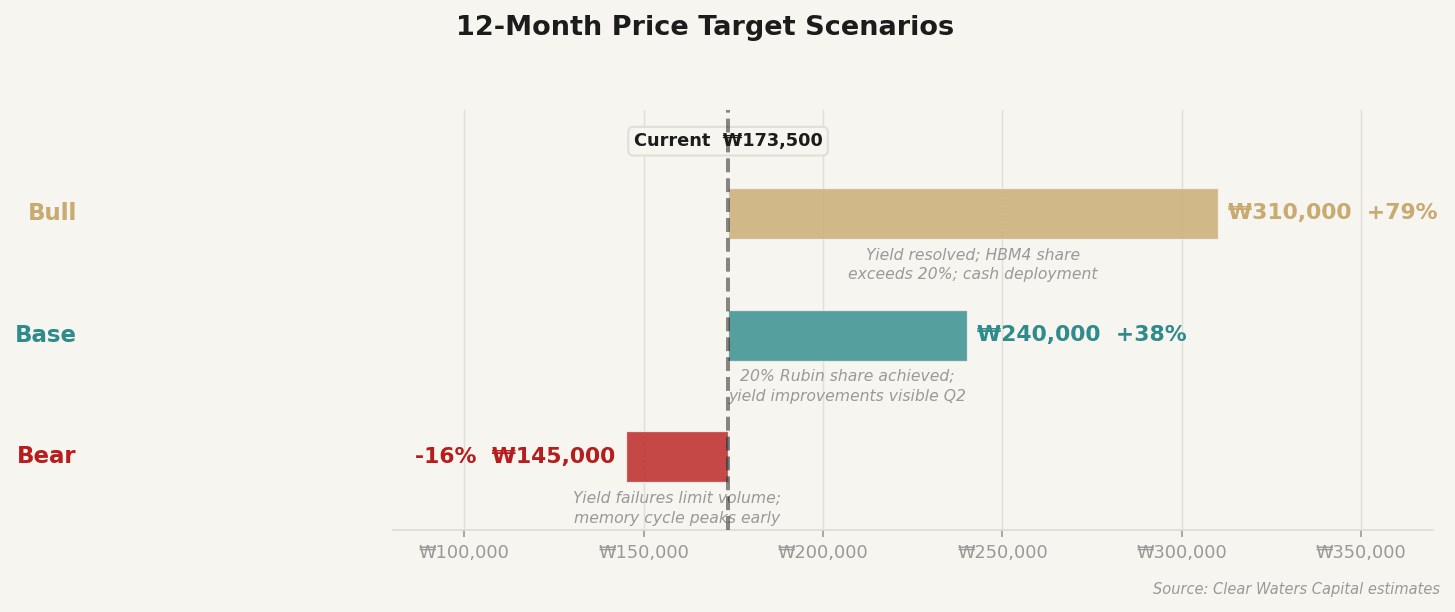

We are focused on directional correctness rather than precise multiples. Our KRW 240,000 target acknowledges an improved earnings bottom while remaining realistic about future growth rates, supported by KRW 100.6 trillion in net cash.

Base case: KRW 240,000 — Driven by execution of the 20% Rubin share and solid internal yield improvements. The overall directional trajectory of earnings provides the buffer.

Bull case: KRW 310,000 — Yield problems fully resolved, HBM4 share expands beyond 20%, and partial deployment of the cash hoard.

Bear case: KRW 145,000 — Compounding yield problems limit shipping volume; memory cycle peaks early. Net cash provides the support floor.

Initiating coverage: Buy. 12-month price target: KRW 240,000. Conviction: Medium-High.

Risks

The central execution risk is stack yield. HBM4 requires stacking 12 to 16 memory dies on top of a logic base die. Samsung chose its bleeding-edge 1C-class DRAM for these layers, which currently yields roughly 50–70%. Even though defective dies are discarded before assembly (KGD testing), the delicate bonding process and TSV connections compound the risk of defects with each added layer — meaning a failure during packaging scraps the entire $700 unit.

SK Hynix took the safer route, using mature 1B-class DRAM with highly stable yields paired with TSMC's proven logic dies. Hyperscale data centers require massive, reliable supply volumes. If Samsung cannot solve its compounding yield issues at scale, its cost advantage becomes a delivery liability. This is why Samsung's base-case share is currently pegged at just 20%.

There is also a macro timing risk: if legacy DRAM pricing peaks before HBM4 shipments fully compensate, margins compress. However, Samsung's 2026 NCNR contracts significantly mitigate this in the short term. The rising supply of legacy DRAM from CXMT presents a notable competitive risk looking into 2027.

Conclusion

What to look out for

1C-DRAM Yield Progression: Per-layer yields must visibly improve toward 80%+ to make stack packaging viable at scale. We await clarity in Q1 earnings, specifically looking for any updates on yield improvements or signals that Samsung might dual-source base dies with TSMC if internal efforts stall.

NVIDIA Rubin Ramp: Industry checks confirming Samsung effectively maintains its 20% base-case HBM4 volume share into H2 2026. Below 20% for two consecutive quarters is a kill condition.

Note on sourcing: Several data points originate from non-public research reviewed in March 2026. Readers should independently verify these figures before relying on them.