Investment Thesis

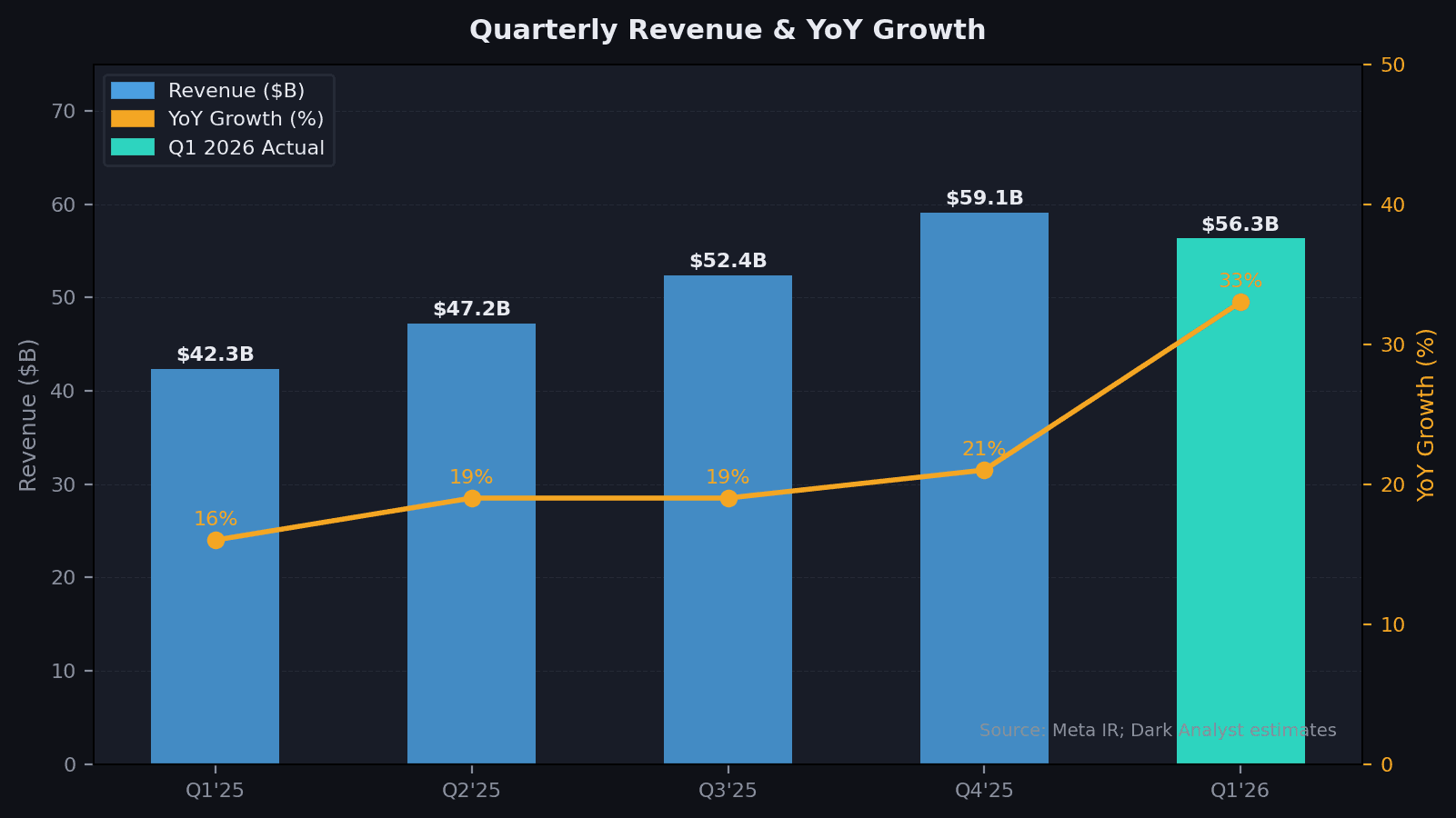

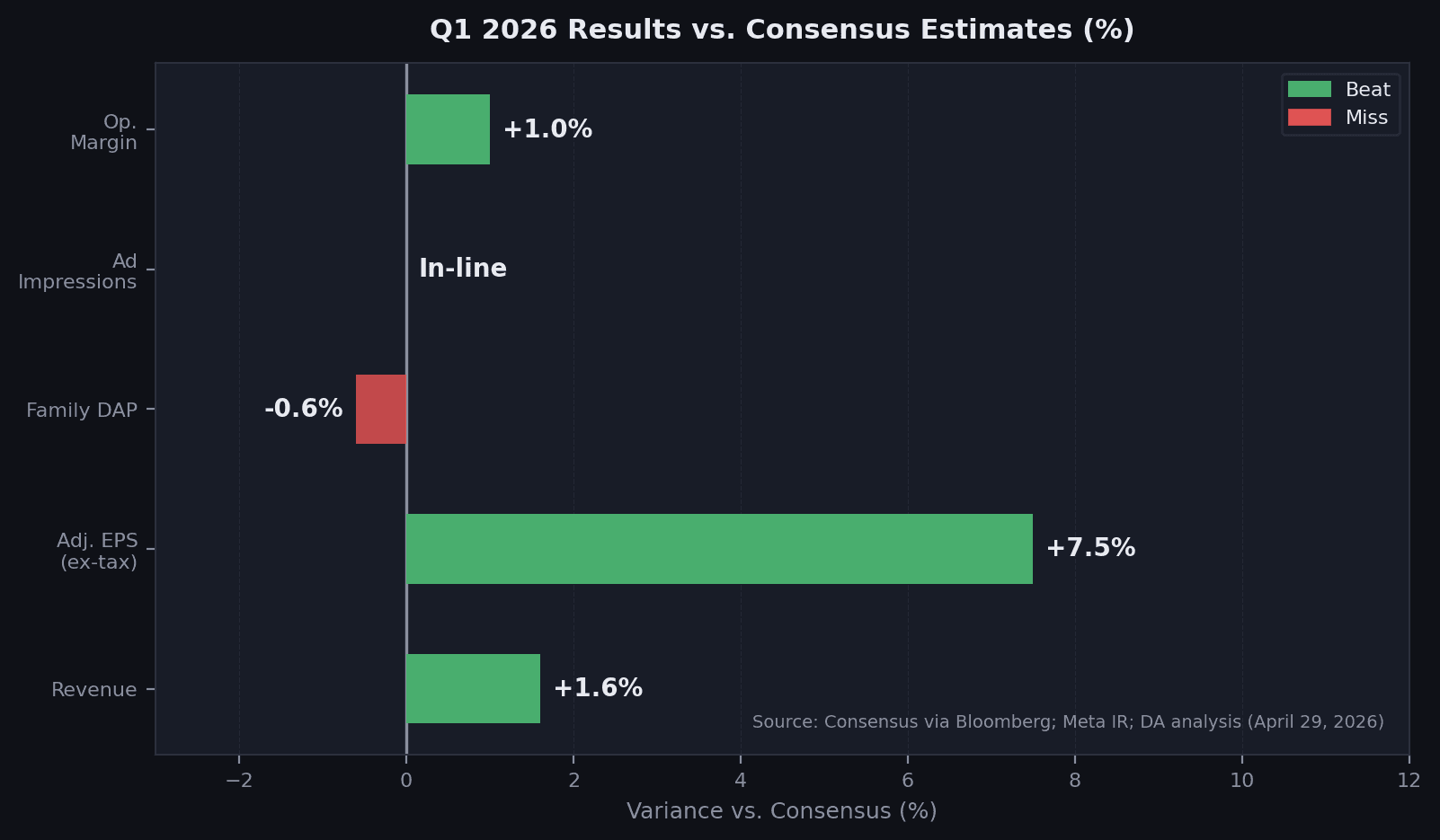

Meta just reported Q1 2026 revenue of $56.31 billion — up 33% year-over-year, the fastest quarterly growth since 2021. Adjusted EPS of $7.31 beat consensus by 8.8%. The stock fell 9%.

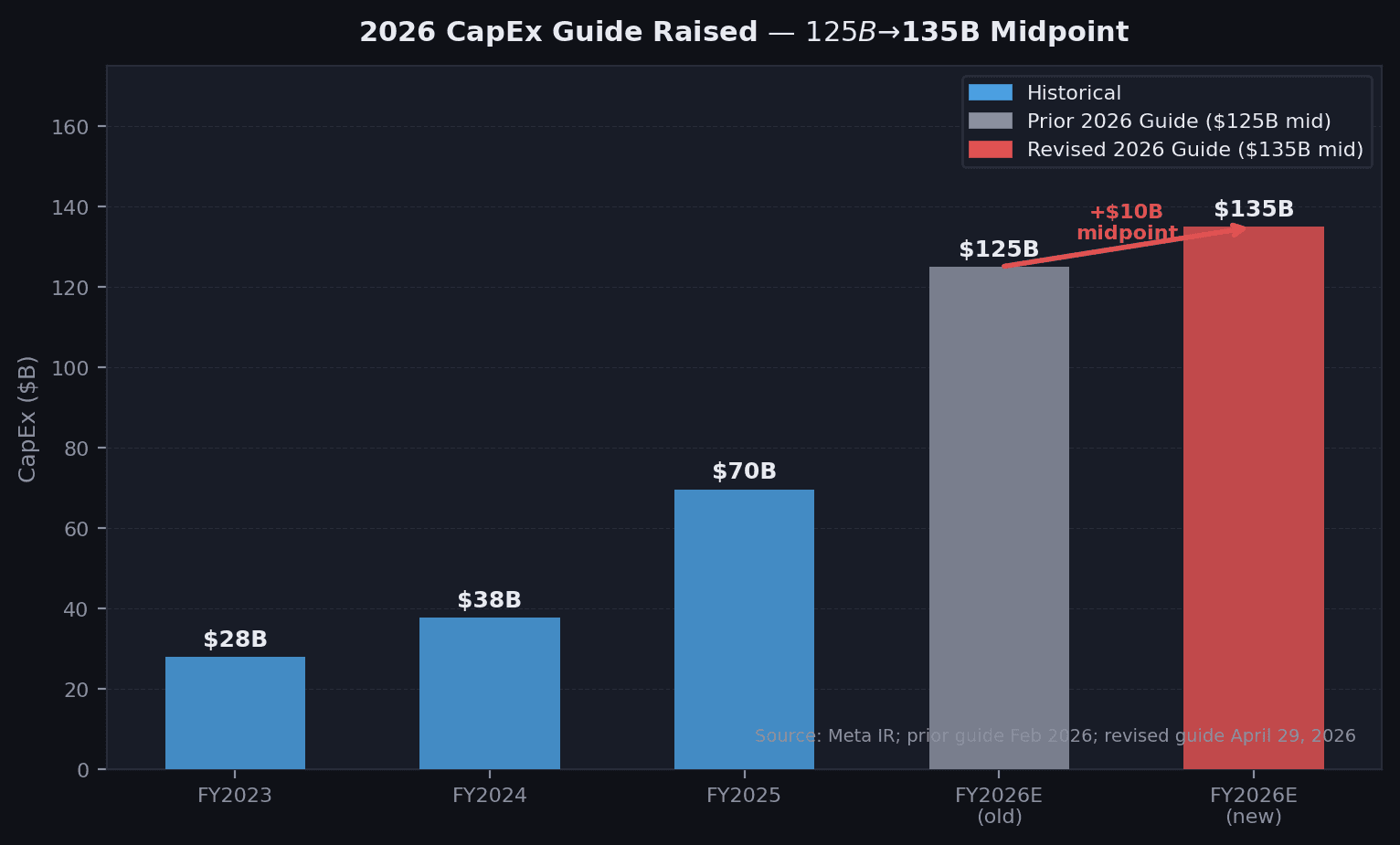

The selloff was driven entirely by a $10 billion midpoint increase in full-year capex guidance, from $125 billion to $135 billion. Management explained it as higher GPU and data center component pricing — compute cost inflation. Google guided $185 billion in capex for the same year. Amazon and Microsoft face the same curve. The market punished only Meta, because Meta has no external AI revenue line. That asymmetry in reaction reveals a structural misreading of what Meta's AI spend is for.

Three things the market is underpricing:

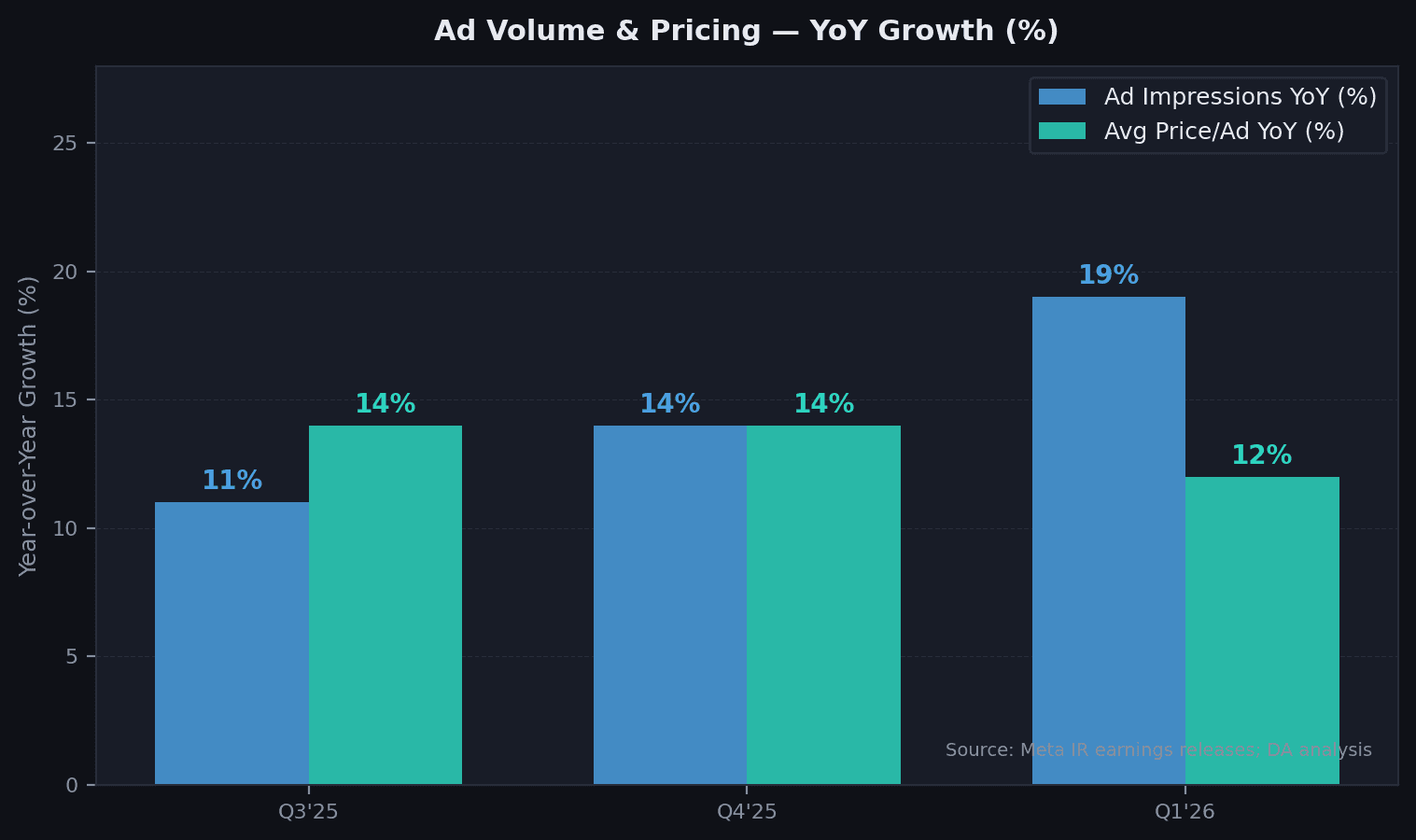

Advantage+ is already generating measurable AI ROI. Ad impressions were up 19% year-over-year in Q1 and average price per ad up 12% — both growing simultaneously, in the same quarter. That combination only happens when targeting quality is genuinely improving. Nvidia CEO Jensen Huang put a number on it in February: cash return on invested capital above 52% on Meta's AI investment. He singled out Meta specifically as the company best at using AI. That is a result, not a forecast.

The data layer is the moat nobody prices. Meta operates three overlapping graphs at 3.56 billion daily user scale: a social graph (who you know), a behavioral graph (what you linger on, share, react to, and buy after seeing), and an identity graph (cross-platform: Facebook, Instagram, WhatsApp, and Messenger simultaneously). OpenAI trains on public internet text. Google has search intent. Amazon has purchase history. Meta has the social layer — the richest signal for predicting human attention and intent that exists. Advantage+ outperforms every competitive ad product because it draws on behavioral patterns observed across four platforms at once. That training data advantage compounds: more users generate richer signal, which improves targeting, which makes the platform stickier.

The capex strategy is correct. Meta owns its training infrastructure — the strategic layer where model weights and IP are created — and leases inference capacity from specialists. The $35 billion CoreWeave commitment ($14.2 billion in 2025, expanded by $21 billion in April 2026 through 2032) handles AI inference delivery for 3.56 billion users globally. US power grid permitting constraints mean Meta cannot build owned inference capacity fast enough — CoreWeave deploys next-generation silicon faster than Meta can permit and construct. Owning the training, renting the commodity is the right split. The $135 billion is not bloated. It is targeted at the layer that generates durable competitive advantage — and at the cost of not depending on OpenAI or Google to run its own products.

Business Overview

Meta's Family of Apps — Facebook, Instagram, WhatsApp, Messenger, and Threads — reaches 3.56 billion people daily and 3.98 billion monthly. It generated $55.91 billion in revenue in Q1 2026 at a 48% operating margin. That margin figure matters for the valuation section: it is higher than Google Services (~35%) at a larger absolute scale.

Reality Labs — the VR/AR hardware and software segment — reported a $4.0 billion operating loss in Q1, down from $5.1 billion in Q4 2025. That improvement is tentative, but it is the first sign of plateau after five consecutive years of escalating losses totalling over $80 billion. Ray-Ban Meta smart glasses, built with EssilorLuxottica and priced at $299–799, tripled in unit sales in 2025. Zuckerberg has guided that Reality Labs losses peaked in 2025. The glasses are where the data layer, the AI model, and the hardware thesis converge — an AI assistant embedded in a consumer wearable that knows its user's social graph.

Financial Analysis

The advertising duopoly. Meta and Google together control more than 50% of the global digital advertising market, which reached approximately $700 billion in 2025 and is growing at 10–12% per year. The two products are complementary rather than substitutable. Google captures search intent — users actively looking for something to buy. Meta captures social attention — users passively scrolling. Advertisers routinely run both. Neither displaces the other, which is why the duopoly has proven structurally durable against every new entrant for fifteen years.

2026 is the year Meta surpasses Google in total global digital ad revenue for the first time, with analyst consensus projecting Meta at approximately 26.8% market share versus Google's 26.4%. The inversion is AI-driven: Reels expanding inventory, Advantage+ expanding yield. Meta is growing into the position of the world's largest digital advertising business while running the highest margins in the category.

AI ROI — the closed loop. Advantage+ automates creative selection, audience targeting, and placement decisions across Meta's surfaces. Advertisers running Advantage+ campaigns consistently report higher return on ad spend than manually managed campaigns — which drives incremental budget allocation onto the platform. Higher budget allocation increases auction density, which raises average CPMs. Higher CPMs generate more revenue, which funds better model training, which improves targeting quality further. The loop is self-reinforcing.

Q1 2026 is the clearest evidence yet that the loop is running: ad impressions up 19% year-over-year and price per ad up 12% simultaneously. The $60 billion-plus annualised revenue run rate on Advantage+ products, with advertiser adoption doubling over the past year, is the monetisation of that flywheel. Jensen Huang's cash ROIC figure of 52% is the external audit of whether it is working.

The capex raise in context. The $10 billion midpoint increase to $135 billion was the sole driver of the post-earnings selloff. Management attributed it to higher input costs — Nvidia GPU pricing and data center component inflation — rather than an expansion of strategic scope. Every hyperscaler is reporting the same cost pressure: Google at $185 billion, Microsoft and Amazon at comparable figures. The difference in market reaction reflects the fact that Google's AI spend creates a directly monetisable cloud revenue line, while Meta's creates better ad products and smarter glasses. The street has not yet built a framework for valuing internal AI productivity at scale.

Meta's own compute architecture reinforces the thesis. The $135 billion in owned capex funds training infrastructure — data centers, MTIA custom silicon, the process of creating model weights. The $35 billion CoreWeave commitment through 2032 funds inference delivery — serving AI results to 3.56 billion users at millisecond latency across geographies Meta cannot build into fast enough given US grid permitting constraints. The split is deliberate. Training is episodic, centralised, and strategically sensitive: own it, control the IP. Inference is continuous, distributed, and increasingly commoditised: rent next-generation silicon from specialists deploying it faster.

Valuation

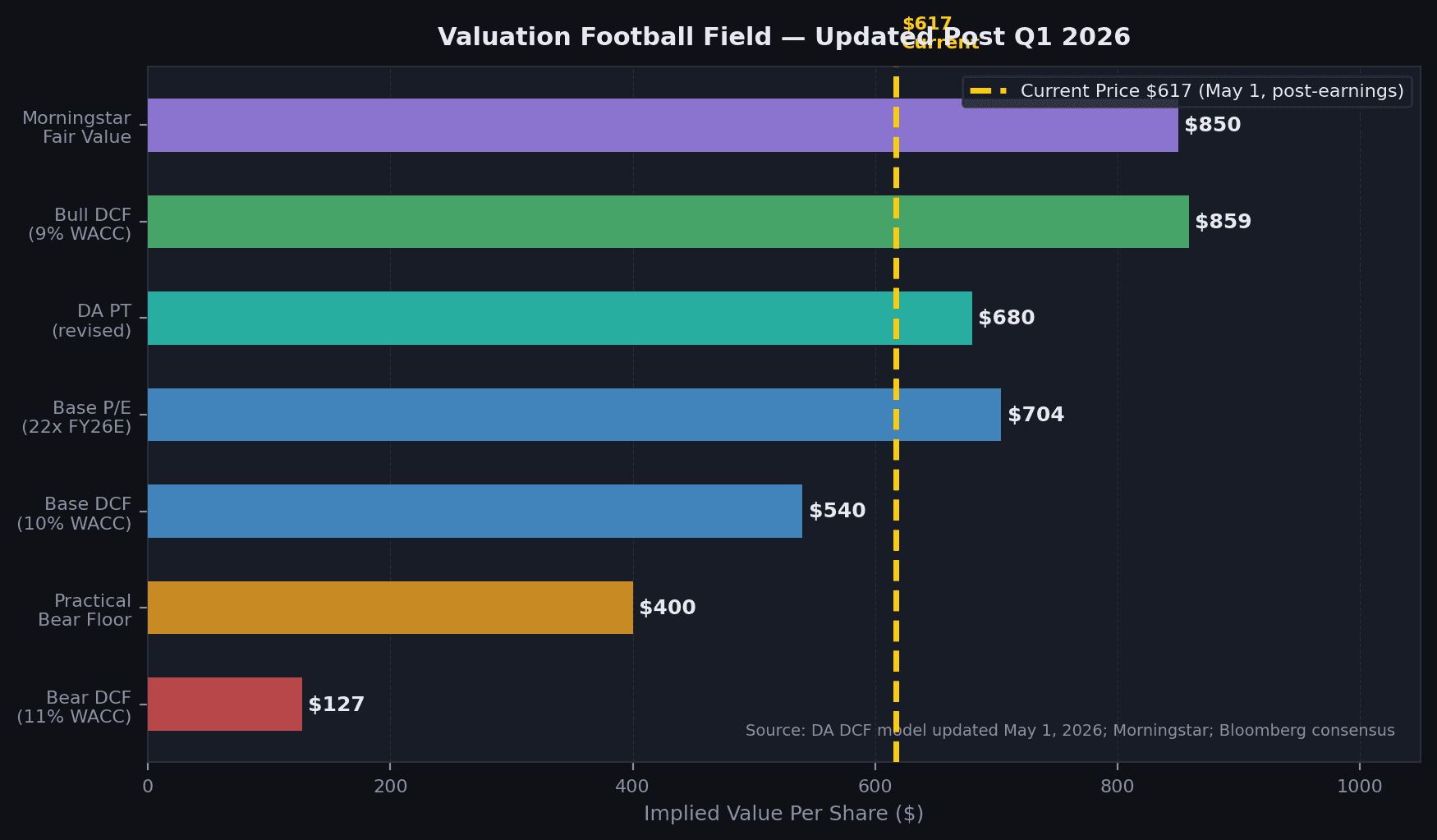

At $609, META trades at 19.1x my revised FY2026E normalised EPS estimate of $32. Alphabet trades at approximately 21x. Meta is the faster-growing, higher-margin advertising business at a discount to its nearest peer on the same earnings multiple.

The revised 12-month price target is $720, implying approximately 22.5x FY2026E normalised earnings — a modest premium to Alphabet that reflects Meta's superior revenue growth rate, higher Family of Apps margin, and the data moat advantage in AI-driven advertising. The prior target of $720 from initiation (April 28) is maintained; the $40 reduction I noted in the immediate post-earnings update reflected excessive weight on near-term FCF compression. At the current price, the multiple discount to Google is the more relevant anchoring fact.

Three scenarios:

Base case: $720 — Advantage+ continues taking share, ad impressions sustain 15%+ growth, Reality Labs losses plateau at or below $18B for FY2026, and the market begins to re-rate Meta toward parity with Alphabet on earnings multiples.

Bull case: $1,050 — AI monetisation beyond advertising begins to show revenue (Business AI agents, smart glasses subscription), Reality Labs losses decline materially toward $14B, and the data-layer/AI-ROI thesis earns a premium over the Alphabet multiple.

Bear case: $400 — Capex ROI fails to materialise beyond Advantage+, Reality Labs losses re-accelerate above $22B, and FCF remains negative through 2028. This requires a genuine capital allocation failure, not just a delayed timeline.

At $609, upside to base is +18%, downside to bear is −34%. The asymmetry is not yet compelling enough to add aggressively. I become a buyer below $580 — approximately 18x normalised earnings and consistent with the low end of the DCF sensitivity range at 10% WACC.

Risks

The frontier model gap — correctly framed. Meta trails Google, OpenAI, and Anthropic at the frontier. The company delayed its flagship model in early 2026 after internal benchmarks fell short of the leading three. Muse Spark, from the newly established Meta Superintelligence Labs, is the stated response — but no external benchmarks have been published. The risk is real, but the framing matters: Meta does not need GPT-5 quality to defend Advantage+ or Ray-Ban Meta. It needs AI that is sticky enough to improve 3.56 billion users' feeds, ad auctions, and wearable assistants. "Good enough" is a lower bar than "frontier" — and the open-source efficiency flywheel makes it a faster-moving target. Llama 4 already follows the DeepSeek V3 mixture-of-experts architecture directly. DeepSeek V4's manifold-constrained hyper-connection techniques, published openly in early 2026, will flow into Meta's next model at zero IP cost. Closed labs must develop comparable efficiencies internally. Meta captures them from the research commons.

FTC antitrust appeal — a known quantity. The district court ruled in Meta's favour in November 2025, finding explicitly that Meta does not hold monopoly power given competition from TikTok and YouTube. The FTC has appealed — a 12–18 month process with an uphill legal argument against an explicit trial finding. Forced divestiture of Instagram or WhatsApp: I assign less than 10% probability over a 24-month horizon. The Google DOJ antitrust case provides the clearest precedent: Google was found guilty of search monopoly in 2024, the remedies have been modest and slow-moving, and Alphabet's stock has compounded through the entire process. Antitrust litigation against platform businesses generates multi-year noise. The advertising compounding continues underneath it.

FCF trough in 2026. Free cash flow is negative this year at approximately −$15 billion — a mechanical consequence of $135 billion in owned capex against approximately $120 billion in operating cash flow. D&A on the 2025–2026 capex build will peak around 2027–2028, after which the capital intensity of incremental AI investment normalises. The stock cannot re-rate on FCF yield before 2028. That is the near-term ceiling on the thesis, and the primary reason this is a HOLD rather than a BUY at current prices.

Conclusion

Meta controls the data, owns the training infrastructure, rents the inference, and runs the highest-margin advertising business in the world at a discount to Google. The Q1 2026 numbers — +33% revenue, +19% impressions, +12% price per ad, 48% Family of Apps margin — confirm that the AI investment is generating returns in the core business today. Muse Spark and Business AI agents represent the next layer of monetisation, but they are not required to justify the current price.

Jensen Huang's framing remains the most efficient summary: Meta is building the organisation best at using AI, not the organisation building the best AI model. Given that Meta sits on a training dataset — 3.56 billion daily users' social graphs, behavioral patterns, and identity signals — that no competitor can replicate, that distinction is worth more than the market currently prices.

What to watch:

- Llama 5 architecture. Does it incorporate DeepSeek V4's mHC efficiency techniques? A Llama 5 with benchmark parity against frontier models at materially lower active parameter count would confirm that the capability gap is closing faster than feared.

- Muse Spark benchmarks. Meta Superintelligence Labs has yet to publish model cards or ArXiv performance comparisons. Any publication benchmarking Muse Spark against GPT-5, Gemini 2.5, or Claude 4 will establish how seriously to take the frontier model narrative.

- Reality Labs FY2026 loss trajectory. If total losses come in below $18 billion (versus $19.5 billion in FY2025), it validates the peak-loss guidance and begins removing a structural earnings drag that has weighed on normalised EPS for five years.

- Business AI monetisation. Zuckerberg has positioned the 10 million weekly Business AI conversations as a future revenue event. Any specific pricing framework or timeline guidance at the Q2 2026 call would establish a new revenue line for modelling that does not currently appear in the base case.

Maintaining coverage: Hold. 12-month price target: $720. Add below $580. Trim above $850.